As a result of the bear market and the recent crises, yields in the crypto market are currently only slightly above fiat money market rates. However, unlike fiat money markets, crypto yields have substantial upside as they are strongly geared to a recovery in the market. Meanwhile – despite media headlines to the contrary – the losses due to hacks and exploits have been steadily declining.

Lower crypto yields reflect reduced demand

Yields fell significantly after the triple crisis of the third largest stablecoin’s failure in May, the string of defaults by centralised crypto lenders in June, and the crypto bear market that dried up demand for financial services in crypto. Many investors who had been able to earn annualised yields of 25 to 40 percent suffered significant losses through unhedged exposures to TerraUSD, exposures to centralised lenders or uninsured hacks.

Consequently, available yields have declined significantly as unsustainably high rates (such as those offered by the Anchor protocol on TerraUSD) have fallen away, demand for loans and volumes on DeFi platforms have contracted, and DeFi protocols are offering less incentives to liquidity providers as their business volumes shrink.

Reduced losses from DeFi hacks and exploits

As the crypto infrastructure matures, the losses from hacks and exploits targeting DeFi platforms have been steadily declining. Based on the list of hacks and the monetary value lost, we find that if we only consider hacks of the DeFi platforms themselves, year-to-date (YTD) losses annualise to 0.49 percent of the average of USD total value locked (TVL) across these protocols. This compares to 1.3 percent in 2021 and 2.26 percent in 2020.

If we also include hacks of interoperability protocols (“bridges”) that connect with DeFi protocols to port assets from blockchains other than the chain the protocol is built on, the losses YTD amount to an annualised 1.01 percent of the average TVL versus 1.82 percent in 2021.

Stablecoin depegging caused an additional approximate 15 percent of losses, however, the reason for the loss to crypto yield investors was their choice not to hedge stablecoins as they regarded the price risk negligible. The same investors would have typically hedged exposure to other crypto assets if they contributed those to DeFi protocol liquidity pools – but stablecoins were typically left unhedged. The resulting loss should be regarded as a risk management failure rather than a crypto yield market failure. Lessons were learnt.

Prudent risk management is of great importance beyond just stablecoins – loss from a given hack may be only a fractional percent of the market’s total TVL, however, a single investor may have 10 to 25 percent of their portfolio in that protocol. Managers with strong risk controls and mitigations have outperformed other managers by a wide margin this year.

Rising fiat interest rates

As central banks around the world have been raising interest rates in response to persistent inflation, the gap between fiat and crypto yields has shrunk further.

The comparison to fiat money market rates is much less favourable today than it was 6 to 12 months ago. If we consider the fragile, and grossly over-indebted, state of most Western economies, it might be worth pondering whether rates, that were considered risk free and used as a basis for comparing yields on more risky traditional investments, are actually “risk free”.

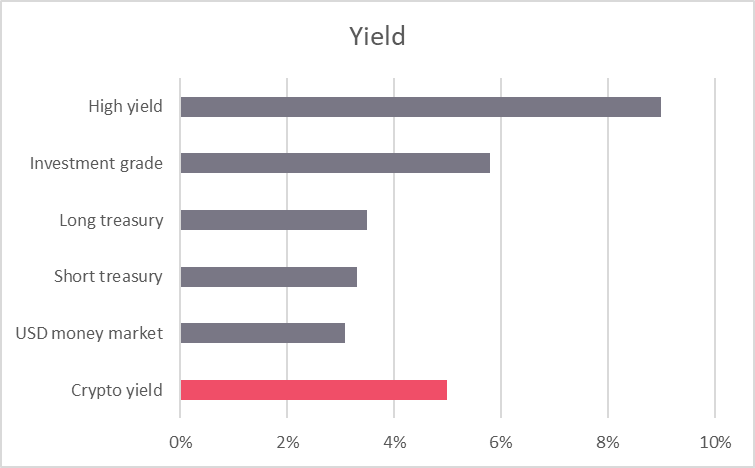

Crypto yields at their current depressed rate fall somewhere between government bonds and corporate bond yields.

Source: High Yield – iShares iBoxx USD High Yield Corporate Bond ETF; Investment Grade – SPDR® Bloomberg Barclays US Corporate Bond UCITS ETF; Long Treasury – Vanguard Long-Term Treasury ETF; Short Treasury – iShares USD Treasury Bond 0-1 yr UCITS ETF; Money Market – SPDR® Bloomberg 1-3 Month T-Bill ETF; Crypto Yield: Sygnum Bank data; all as of 30 September 2022

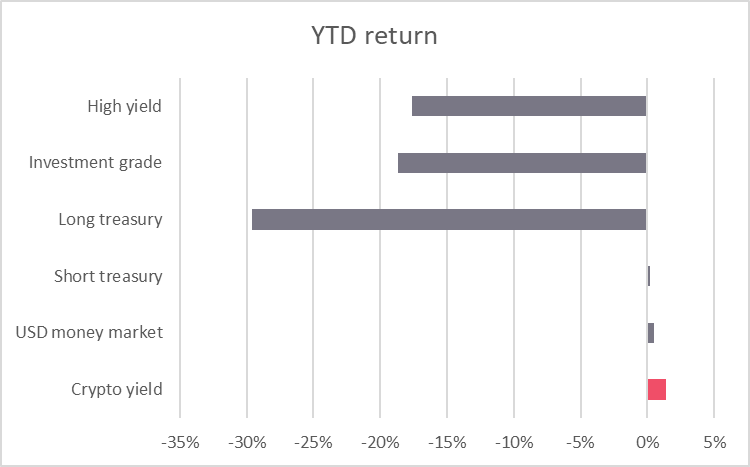

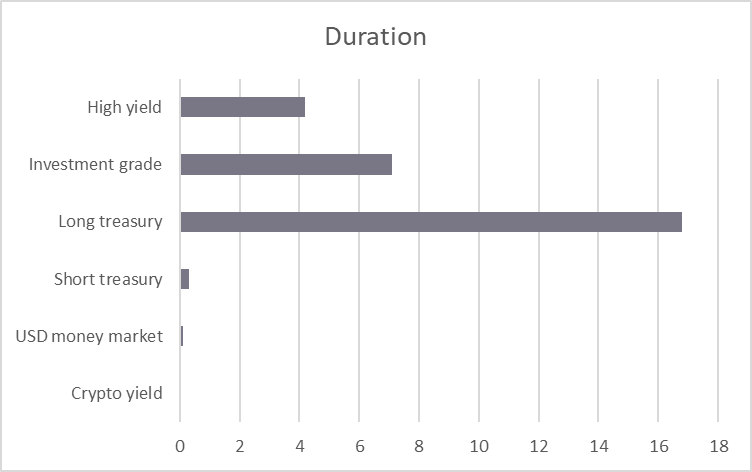

Although corporate bonds offer somewhat higher yields currently than crypto, they have significant price risk. Crypto yield investments have a duration of close to zero and bear no price risk. The year-to-date performance of high-yield and investment-grade bonds and longer-dated treasuries is in deeply negative territory, with returns between minus 17.5 percent and minus 30 percent.

Meanwhile, crypto yields are estimated to remain in slightly positive territory year-to-date when we use the proxy of typical underhedged and uninsured returns prior to May and the typical (much lower) returns since May, and subtract the value of the hacks, exploits and other losses (including losses from TerraUSD and hacks on interoperability bridges). The better managers have been able to outperform this proxy.

Outlook

Crypto yields currently offer a small (1.5 to 2 percent) incremental yield over USD money market and treasury bonds, with no duration risk. Losses from hacks and exploits are currently comparable to the default rates on corporate bonds at the lower end of investment grade (around BBB+). While such losses have been declining, default rates in the traditional markets are likely to increase as slower growth puts pressure on revenues, inflation pushes up costs and refinancing liabilities becomes much more expensive.

As the risks associated with crypto yields (such as the technology or maturity of projects and the sector) are different from the value drivers of traditional yields (which include monetary policy or the business cycle), they are a good diversifier for yield portfolios.

Additionally, crypto yields have substantial upside when the crypto market recovers as the demand for various decentralised financial services (such as DeFi lending and decentralised exchanges) will grow. It is also very likely that in a bullish environment, projects will again aggressively vie for market share by providing attractive incentives, and with more activity, there are typically also more inefficiencies that the best yield investors can exploit.

To be the first to get the latest news on Sygnum and the market, expert insights and industry research please follow us on Linkedin and Twitter.

About Sygnum

Sygnum is the world’s first digital asset bank, and a digital asset specialist with global reach. With Sygnum Bank AG’s Swiss banking licence, as well as Sygnum Pte Ltd’s capital markets services (CMS) licence in Singapore, Sygnum empowers institutional and private qualified investors, corporates, banks, and other financial institutions to invest in the digital asset economy with complete trust. Sygnum operates an independently controlled, scalable, and future-proof regulated banking platform. Our interdisciplinary team of banking, investment, and Distributed Ledger Technology (DLT) experts is shaping the development of a trusted digital asset ecosystem. The company is founded on Swiss and Singapore heritage and operates globally. To learn more about Sygnum, please visit www.sygnum.com.

Disclaimer

This document is purely for educational purposes and has been issued by Sygnum Group. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a marketing communication. It does not constitute an offer or a recommendation to subscribe, purchase, sell or hold any security or financial instrument. It contains the opinions of Sygnum Group, as at the date of issue. These opinions and the information contained herein do not take into account an individual‘s specific circumstances, objectives, or needs. No representation is made that any investment or strategy is suitable or appropriate to individual circumstances or that any investment or strategy constitutes personalized investment advice to any investor. Therefore, you must verify the above and all other information provided in the document or otherwise review it with your external advisors. Some investment products and services, including custody, may be subject to legal restrictions or may not be available worldwide on an unrestricted basis. The information and analysis contained herein are based on sources considered as reliable. Sygnum Group uses its best efforts to ensure the timeliness, accuracy, and comprehensiveness of the information contained in this document. Nevertheless, all information indicated herein may change without notice.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.