Many traditional financial companies and crypto-native firms spent the last 12 months fortifying their foundations for tokenization and exploring different ways to represent and trade real-world assets (RWAs) on blockchains.

The tokenized market has graduated from being a niche experiment to enjoying widespread adoption by the likes of BlackRock, Fidelity and an impressive list of major global banks fully committed to bringing capital markets on-chain. The growing market has also established specialised tokenization chains, such as Ondo Chain.

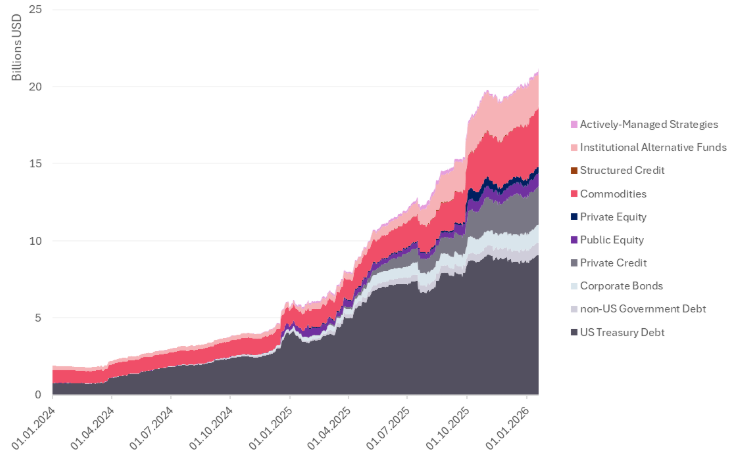

Total RWA value on decentralised blockchains

Source: RWA.xyz (excl. public, permissioned RWA value and stablecoins)

The result of this increased innovation was a 250 percent rise in the volume of freely tradeable RWAs issued on decentralised networks with a value of nearly USD 22 bn by start of 2026. That figure may pale in comparison to traditional asset classes, but volumes are growing fast.

In addition, there is a much larger market volume of financial instruments that have technically been tokenized but are held by institutional custodians, largely on the public permissioned infrastructure Canton Network rather than being freely circulated on decentralised rails such as Ethereum and Solana (see section below). Alongside the growth of on-chain RWAs in 2025, the DeFi payments layer also witnessed a 50 percent increase in the value of stablecoins in circulation (around USD 300 bn).

The last 12 months also revealed clearer adoption drivers for tokenized RWA projects as different approaches emerged across several asset classes. But regardless of approach, the attractions of tokenization include cost savings by removing intermediaries, near-instant transactions 24/7, and in some cases increased liquidity in the financial markets, unlocking the value of assets through fractionalisation and using RWA-backed tokens for trading, lending collateral, and even dividend distribution. An additional (but still early) attraction is the move toward a programmable value chain that will automate parts of the asset life cycle.

However, there are still some remaining bottlenecks that prevent the floodgates of tokenization from fully opening. These chiefly sit in the realms of regulation, taxation and KYC/AML. The progress, or lack thereof, of the CLARITY Act in the US will determine in large measure the future velocity of progress in the market.

The current state of tokenization

The tokenized RWA market matured considerably in 2025, driven mainly by large institutional players, such as Blackrock and Fidelity, that have built on earlier forays into the market, such as tokenized Money Market Funds and ETFs. For instance, a Blackrock executive recently announced that the iShares Bitcoin ETF product suite had become the most profitable product line for the world’s largest asset manager.

The volume of tokenized US treasuries, from all issuers globally, grew 136 percent during the course of 2025 to USD 9.33 bn. BlackRock’s BUIDL leads market share at USD 1.7 bn, but Circle’s USYC is aggressively catching up (USD 1.5 bn) since its native launch on BNB Chain and Binance support for developer and institutional collateral use.

If 2024 was the year of the first crypto-backed ETFs, 2026 could see the launch of tokenized ETFs that would make shares in ETFs available via decentralised trading. Institutional heavyweights like BlackRock and crypto-native companies like Kraken and Ondo are making this a strategic priority.

Franklin Templeton has received clearance from the Luxembourg financial regulator to issue a fully tokenized UCITS fund. Bitwise has filed in the US to launch a combined stablecoin and tokenization ETF that would provide exposure to an index of stablecoin issuers, tokenization infrastructure and regulated Bitcoin and Ether ETPs.

Meanwhile, tokenized equities reported record high levels in recent months, in part reflecting the strong performance in public equity markets. Quarterly volumes reached nearly USD 5bn, with close to half of that activity happening in December alone. BNB Chain now dominates traded flows after Ondo Finance launched its Global Markets platform for Binance users. Since the launch of Backed Finance’s xStocks in June last year, tokenholders have increased by a substantial 46x, while a similar trend is happening with tokenized commodities due to gold and silver’s outperformance, with tokenholders rising 2x since early last year to 188k.

The tokenization progress witnessed over the last months has helped result in more than USD 350 bn of RWAs being technically on-chain, custodied by large traditional institutions on permissioned blockchains, but not distributed for trading in a decentralised manner. A substantial share of this activity consists of tokenized repurchase agreements (repo) held on the Canton Network, which have arguably found product-market fit in institutional funding and collateral markets.

The collaboration between the Canton and the Depository Trust & Clearing Corporation (DTCC), which is slated to go live in H1 2026, sends a strong signal that the scale of tokenized RWAs could be set to mushroom.

Public, permissionless vs permissioned or parallel growth?

Ondo Finance’s Ondo Chain and Digital Asset’s Canton Network are prime examples of established financial heavyweights seeking to make capital markets more efficient through tokenization on public, permissioned networks. The primary goal is to make existing market structures faster and more efficient using distributed ledger technology.

Such permissioned networks are the most regulator-friendly, offering the ability to limit participation to institutional players and to conduct KYC/AML procedures. This system is also more useful for keeping the details of transactions confidential, which is critical for participants who do not want to reveal their strategies. This is ideal for activities such as the repo markets, which have been successfully tested using the technology.

But the advantages of open permissionless blockchains, such as Ethereum or Solana, are considered more suitable for other RWA tokenization use cases, where access to DeFi liquidity and the broader crypto ecosystem becomes a source of innovation and unique investment opportunities. These include tokenized funds, equities, commodities, private credit, and even fractionalising real estate.

The decentralised network leader in tokenized RWAs is currently Ethereum with USD 12.8 bn on-chain (including around USD 5 bn in tokenized US treasuries), followed by BNB Chain (USD 2.0 bn) and Solana (USD 1.1 bn). All the decentralised networks combined are home to nearly USD 22 bn in tokenized RWAs.

Although this is dwarfed by the USD 350 bn plus held on permissioned rails, and given the sheer size of potential tokenized assets that already trade through traditional market infrastructure, this leads to the opinion that Canton Network is likely to grow at an even faster pace, though largely within these closed settlement and funding use cases.

There is potentially a third path for the market’s development where permissioned networks are used for the primary issuance of tokenized RWAs, which are then bridged to permissionless chains for secondary trading and integration with DeFi protocols. This is also why R3’s private Corda Network decided to partner with the Solana Foundation to bridge its RWA platform to Solana’s permissionless network.

However, the future roadmap for tokenized RWAs will be heavily influenced by regulatory developments, particularly in the US.

Regulation will drive additional flows

The US has already passed a law regulating stablecoins, but a key piece of regulation, the CLARITY Act, has stalled in the Senate, despite having been signed off by the House of Representatives last year. The bill is the second major pillar of crypto regulation in the US, the world’s largest financial centre that has a profound influence on the rest of the world.

The bill intends to define crypto tokens as either securities, commodities or other categories. This would determine where the Securities and Exchange Commission (SEC) or the Commodity Futures Trading Commission (CFTC) has regulatory jurisdiction. US lawmakers are also seeking to lay down the legislative framework of KYC and AML as applied to crypto assets.

But the CLARITY Act has recently ground to a temporary standstill in the Senate with representatives from the crypto industry, such as Coinbase, claiming that proposed amendments would harm innovation and crypto companies. They object to potential restrictions on tokenized equities, a weakening of financial privacy in DeFi, a perceived imbalance of regulatory power toward the SEC, and proposals to limit yield-generating stablecoin models – the latter which has intensified tensions between crypto firms and banks.

There is currently no clear signal of how or when the impasse can be resolved, but the Trump administration and SEC chairman Paul Atkins appear to remain supportive of the crypto industry.

APAC is also reporting a lot of progress in tokenization. In Singapore, Standard Chartered launched blockchain-based deposits in SGD and USD to facilitate on-chain treasury and settlement for institutional clients. DBS and Franklin Templeton launched a tokenized retail money market fund (one of the first regulated retail funds in the region).

Meanwhile, Japan’s regulators have cleared major securities firms and banks to start trading tokenized shares this year, while several banks now offer tokenized deposit services in Hong Kong. And Australia has launched draft legislation aimed at granting licences to tokenization projects later this year.

Outlook

Many participants in both the crypto and traditional finance industries believe in the potential of tokenization to enhance the markets, a view that is now firmly embraced by institutional heavyweights.

“Every stock, every bond, every fund – every asset – can be tokenized. If they are, it will revolutionise investing,” Blackrock chairman Larry Fink wrote in his annual letter to investors in December.

Intercontinental Exchange, the parent company of the NYSE, is also convinced by the benefits of tokenization. It has developed a platform for the 24/7 trading and on-chain settlement of tokenized securities, and together with NYSE is currently seeking regulatory approvals. State Street also announced the launch of its own tokenization platform.

Meanwhile, on-chain data sources show signs that both traditional investors and crypto users are increasingly interested in these kinds of assets. The number of holders of tokenized RWA products increased more than sixfold to 620k over the past year.

The most significant growth is currently being led by traditional institutions, but this does not necessarily mean the retail market will miss out. The popular trading platform Robinhood and Revolut are among the retail-facing companies that are investing in (and offering) tokenization services.

It is also important to note that most major TradFi firms are increasingly launching tokenized offerings on permissionless rails like Ethereum, Solana, BNB Chain, Stellar, Arbitrum and Avalanche, among many others, while emerging models like RWA-backed lending through Aave’s Horizon and Morpho are beginning to turn tokenized RWAs into productive collateral.

As the rest of the crypto market seems to be struggling for direction right now, tokenization is one of the most important trends to monitor this year.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.