The corporate appetite for Bitcoin is usually described as an accelerating treasury trend, but the trend is narrower than it looks and the financing behind it more substantial. Strategy (Nasdaq: MSTR) has issued five preferred stock instruments to fund its Bitcoin purchases, grouped them under the label “digital credit”, and watched a handful of smaller companies replicate the same model. They are often dismissed as leveraged Bitcoin bets in a fixed-income wrapper, which is economically accurate but underrates how well they have worked and leaves the hard question unanswered: under what conditions do they stop working?

Almost entirely Strategy

No company holds anywhere near as much Bitcoin as Strategy. It owns roughly 843,700 BTC, close to 4 percent of all the supply that will ever exist, bought for approximately USD 63.9bn at an average cost basis of around USD 75,700 per coin. Only a handful of governments hold more than the largest of the other companies, and their Bitcoin came mostly from seizure (not deliberate purchases), which leaves them outside the trend. The other companies are mostly miners, exchanges, or crypto investment firms, for which Bitcoin is part of the business itself.

This leaves only two genuine imitators, Metaplanet in Japan, which holds around 40,000 BTC, and Strive, with around 16,500, both having raised capital to fund their purchase the same way Strategy does.

But these purchases were never going to come from operating cash flow, as Strategy’s software business is far too small to fund buying on this level. The money has instead come through the capital markets, using instruments far more complicated than the plain equity it started with. Strategy raised more than USD 25bn last year, making it the largest equity issuer among US public companies for the second consecutive year.

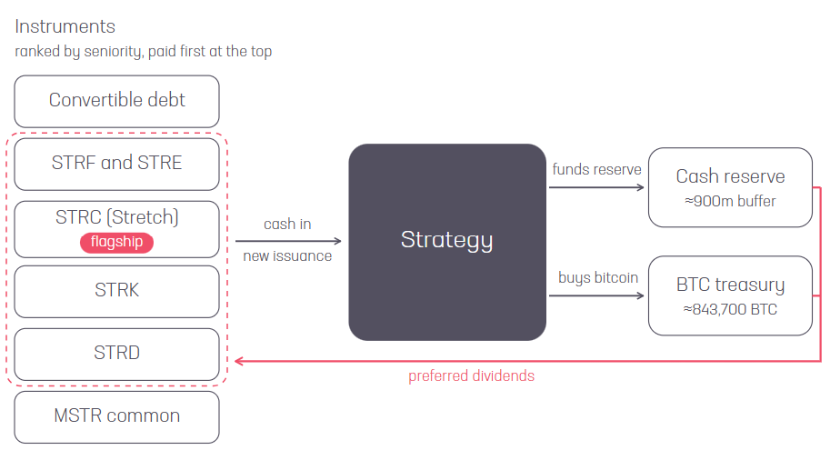

Strategy’s capital flow loop

Source: Strategy, Sygnum Bank

From equity to credit

Strategy’s financing began with common equity, sold through at-the-market (ATM) programmes. Selling new shares would normally dilute existing holders, but here it did the opposite because the shares traded above their net asset value (NAV) – the value of the Bitcoin held per share. Each share sold raised enough to buy more Bitcoin than it cost in dilution, and every raise left existing holders with more Bitcoin behind each share, not less. The advantage depends on the premium, and it narrows as more shares are issued.

Convertible notes postponed the dilution but couldn’t avoid it, since they can convert into shares. As debt, they carried maturities and repayment dates that limited how long the buying could continue.

Perpetual preferred stock removed both constraints at once. Like any preferred stock it ranks below the company’s creditors but ahead of the common shareholders, and pays a dividend instead of a share of profits. Its perpetual form means it has no maturity date, so Strategy never has to repay the principal, and its higher rank lets the company raise money without diluting its existing shareholders.

The company is also under no obligation to pay the dividend, and when it doesn’t, the unpaid amount usually accrues as a balance owed to the preferred holders. Skipping a preferred dividend triggers no default (while skipping a bond coupon would), so in a market downturn Strategy can simply pause the dividend and conserve its cash. A borrower cannot do this.

How the instruments work

STRC is Strategy’s flagship and the largest of the five. The board resets its dividend rate every month to keep the shares trading near their USD 100 par value. When the price slips below par, the board raises the rate, and the higher yield pulls buyers back until the price recovers. The rate has climbed from 9 percent at its launch in July 2025 to 11.5 percent by March 2026 and has held there since. It has never been cut, and when demand is strong Strategy simply issues more shares to fund Bitcoin instead of lowering the dividend. Holding the rate this high is expensive, with Strategy alone paying for it.

Auction-rate preferred securities once worked on the same principle, with their rate reset at regular auctions to hold the price near par. They traded as cash equivalents for years, largely because the banks running the auctions stepped in to buy whatever went unsold. This worked until the 2008 credit crisis, when the banks ran short of capital and stopped bidding, and with no one left to absorb the unsold paper, the auctions could no longer clear, and more than USD 300bn of paper froze.

STRC holds near par with the same rate mechanism, but without the same vulnerability. Unlike an auction, it trades freely on Nasdaq and cannot simply fail to clear, and a holder who wants out can still sell at a lower price. Strategy, for its part, does not step in to buy the shares when they slip below par, and it does not need to. So far, the buyers have kept coming.

STRC has grown into a USD 10bn instrument, trading around USD 375m a day, and though it launched only last summer, USD 5.6bn of the total was raised in the first four months of 2026 alone, and all of it during a Bitcoin downturn.

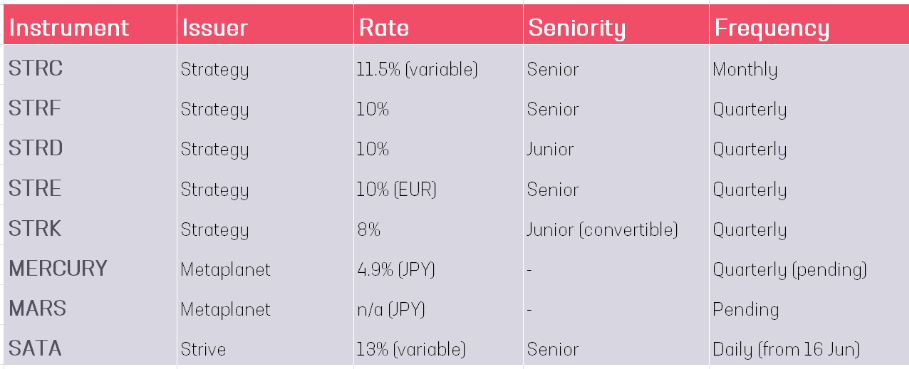

Digital credit instruments by issuer and rate

Source: Strategy, Metaplanet, Strive

Strategy now has five of these instruments outstanding, from STRK at 8 percent to STRC at 11.5. They are all structured slightly differently so that between them they reach almost every kind of income investor, and by extension give Strategy a funding market of its own. For instance, STRK can convert into common stock and the most junior STRD is non-cumulative, so a skipped dividend there is simply lost.

What the market charges for that money has since risen. STRK pays a fixed 8 percent, which only yields more as the share price falls. With STRK down to around USD 74, that yield is now nearly 11 percent for a new buyer. Strategy still pays just 8 percent on the STRK it has already sold, but that higher yield is what new money now costs. The same holds for STRC, whose monthly rate has climbed to 11.5 percent.

Other digital credit adopters

Strive (NASDAQ: ASST) is the closest adopter of the model. It holds around 16,500 BTC, funded by a single instrument called SATA, and carries no debt at all. SATA started at 12 percent and has since risen to 13, which is a full 150 basis points above STRC. Part of that pays for the main selling point, as from June 16 it becomes the first listed US security to pay a dividend every business day, which compounds to approximately 13.9 percent a year.

The rest is a risk premium, as Strive offers the same deal as Strategy on a fraction of the Bitcoin and a far shorter track record – the spread would likely narrow if, and when, Strive shows the model can hold through a sustained downturn.

Japan’s Metaplanet, which holds around 40,000 BTC, has two yen-denominated instruments of its own, a fixed 4.9 percent issue called MERCURY and an adjustable one called MARS, but it has had to delay both. Strategy’s model needs continuous issuance and frequent repricing, and the Japanese market offers neither. ATM share sales are generally barred, and dividends come only once or twice a year.

MERCURY’s 4.9 percent looks meagre beside STRC, but for a yen investor it is actually high. Japanese bank deposits pay almost nothing, and even a 10-year government bond yields only around 2.5 percent, so a fixed yen return close to 5 percent is a rare thing to find.

Whether Strategy’s “digital credit” becomes a global model remains to be seen. The structure it depends on is heavily US-based, and not every market is built for it. Strategy has listed one fixed-rate euro version (STRE) in Luxembourg, and Japan so far none at all.

Does the maths hold?

The strongest objection to all of this has nothing to do with law or regulation. It comes down to one question, and that is whether Bitcoin appreciates faster than the dividend bill, which is around 3 percent of the holdings a year at today’s price. While that holds, the premium holds with it, and Strategy can keep issuing to fund the dividends without ever touching the principal. When it does not, the company must find the cash some other way – by depleting its cash reserve, issuing more stock in a weak market, or in the worst case, selling Bitcoin.

With Bitcoin’s poor performance this year and the market starting to question whether the dividends could be paid out without fresh issuance, Michael Saylor used the Q1 2026 earnings call to show that Strategy could sell a portion of its Bitcoin to cover the dividends (even though Strategy has no need to do so now). The amount was about 2.2 percent of the holdings (the annual dividend bill at the price then), yet the suggestion alone was enough to push the common stock down 4 percent that day. What likely unsettled investors was the possibility that selling might one day stop being a choice. In late May, Strategy made its first sale, a symbolic 32 BTC for around USD 2.5m.

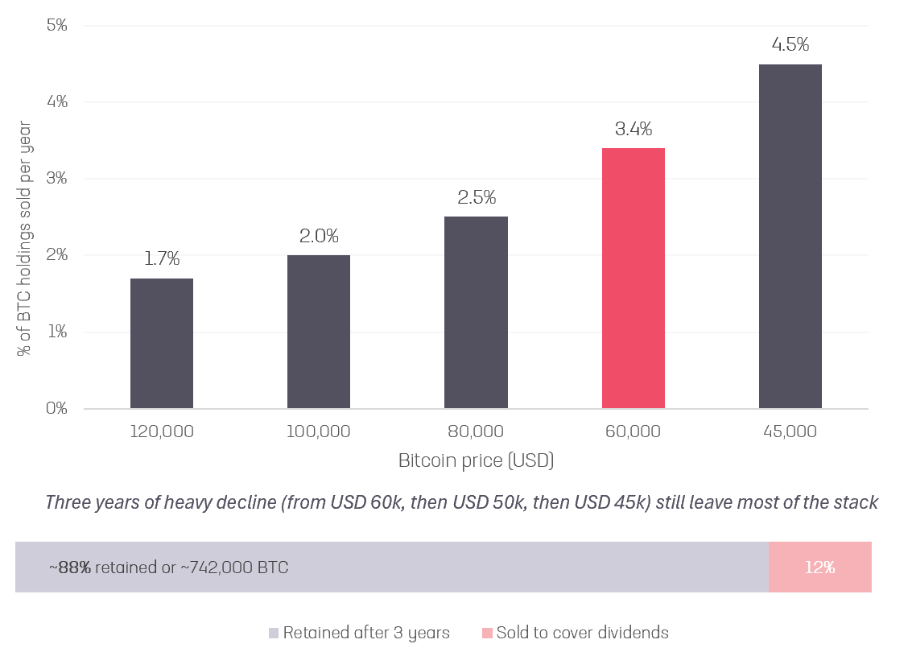

Strategy could withstand a single sharp fall in Bitcoin’s price. The concern would be a decline that drags on without reversing, and one that keeps the issuance window shut. With no fresh capital coming in, the preferred bill of over USD 1.7bn a year could be met only by selling Bitcoin.

Share of BTC stack sold in a year to cover the dividend bill (if issuance stops)

Assumes a ~USD 1.7bn annual preferred dividend bill and 843,738 BTC held (Strategy 8-K, 25 May 2026). Source: Strategy, Sygnum Bank

But the burden is far smaller than it looks. At today’s USD 63,400, a year of dividends comes to about 3 percent of the holdings, and even a substantial fall to USD 45,000 would take only 4.5 percent. The strain is somewhat worse than that, since the bill grows with every new issue of preferred and the STRC rate climbs as Bitcoin falls, but even so the holdings would outlast any drawdown. The premium is the real vulnerability.

The same premium that drove the accumulation can also drive it in reverse. Issuing common shares above NAV only works while the premium holds, and as it narrows, each new share raises less and the cost of capital rises, slowing the buying, which in turn lets the premium narrow further still. The common stock is trading at 1.19 times NAV today.

STRC raises on its own rate and has kept selling as the premium narrowed, but if the buying stops, the dividends have to be funded from cash, or from selling Bitcoin. Strategy set aside USD 2.25bn around the turn of 2026, enough to cover well over a year of payments at the bill the preferred stack now carries. However, in May Strategy spent USD 1.38bn of that buying back convertible debt at a discount, which it had flagged in advance as part of a plan to clear the debt, leaving roughly six months of runway (around USD 900m) and around USD 6.7bn of convertibles outstanding. These are senior to the preferred and must be repaid or refinanced. Meanwhile, the bill will keep growing as STRC expands.

Outlook

None of this, however, is really a question of survival. The dividends can always be met by selling a small fraction of the holdings, which are substantial to say the least. The difficulty lies in the option having been closed off from the start, since the premium was built on the promise never to sell, and a promise that rigid leaves no room to do the sensible thing when conditions require it. The premium is the only thing that makes Strategy worth more than the Bitcoin it holds, and a treasury that sells to fund its yield is no longer what many investors signed up for, at least not while the underlying collateral is in a drawdown.

The model has worked well enough that others are now adopting it, and for income investors it has opened a market that did not exist before, a fixed-income route into Bitcoin paying double-digit yields. How those yields hold up over the long run will come down to one thing no issuer controls – Bitcoin’s long-term performance, which history shows has recovered from every previous decline.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.