Traditional assets have outperformed crypto over the last several months, with gold and silver initiating the outperformance ahead of expected geopolitical tensions that have now materialised with the US/Israel/Iran conflict. High-beta tech stocks also performed strongly, and equities markets more broadly over the same period. Meanwhile, altcoins have been butchered, with many down 80-90 percent from their cycle highs.

This is perhaps why we are now witnessing a shift in the form of crypto exchanges (both centralised and decentralised) offering exposure to traditional assets, with volumes now reaching impressive levels as crypto traders appear to be hedging war and geopolitical tensions through 24/7 oil and precious metals trading activity.

The question is whether this is the beginning of a fundamental shift towards trading traditional assets on blockchain rails or simply a temporary phase until the crypto market begins to show signs of recovery.

The rise of traditional asset perpetuals

Most of the attention is, and rightfully so, on Hyperliquid’s HIP-3 markets, which went live in mid-October and allows developers to launch custom permissionless perpetual markets (they can do this by staking 500k HYPE tokens as collateral).

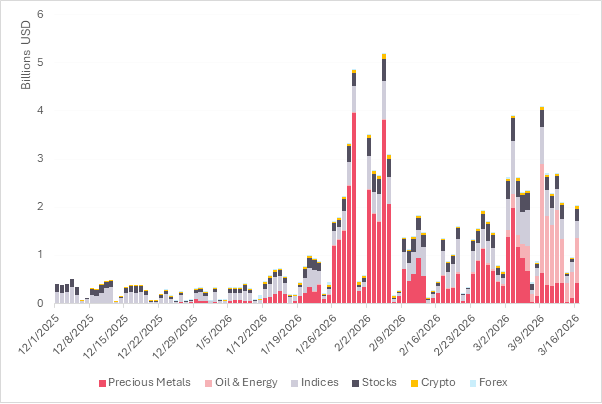

The XYZ100 (Nasdaq 100) perp was the first and dominant HIP-3 contract, reaching over USD 500M in daily volume within weeks and accounting for most of the early activity. However, as precious metals and oil contracts were listed, the composition of HIP-3 volume has changed substantially, with trading volumes accelerating in light of the recent war escalations. Oil and precious metals now account for over 67 percent of volume while indices have fallen to roughly 17 percent.

HIP-3 markets by asset category

Source: Hyperliquid, Loris Tools

Gold and silver were the first major commodities to list on HIP-3 in mid-December. Oil contracts followed in January and Brent Oil in early March. S&P Dow Jones Indices also this week licensed the S&P 500 to Trade.xyz, which is currently the largest HIP-3 marketplace built by Hyperliquid’s tokenization division (Hyperunit), and accounts for approximately 90 percent of all HIP-3 open interest and traded volumes.

Oil perps now dominate HIP-3 activity

Hyperliquid’s CL-USDC oil perps allow traders to go long or short on WTI crude oil using USDC as margin. The conflict in the Middle East led to supply disruptions in the Strait of Hormuz, through which approximately 20 percent of global oil passes daily, and a substantial 30 percent spike to USD 120 per barrel followed the subsequent raids against oil and gas facilities in the region. The surge in oil prices drove 24-hour oil perp trading volumes to nearly USD 2.3B, briefly passing Ethereum perps.

Traditional oil markets close overnight and on weekends, and with much of this conflict playing out outside of market hours, on-chain perps have been the only way to hedge in real time.

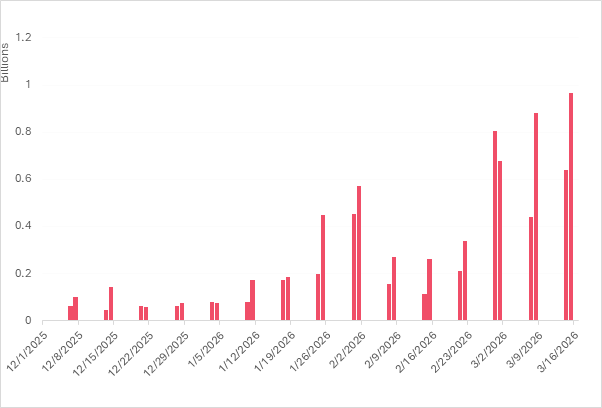

HIP-3 weekday volumes have grown substantially, but it is also worth noting that weekend activity is also growing (up 9x since the first week of Jan). This is likely due to an uptick in crypto-native traders rotating into traditional assets as the broader altcoin market continues to underperform.

HIP-3 weekend trading volume (USD)

Source: Hyperliquid, Dune

These new “micro markets” are now growing into serious trading activity and accruing fees, thereby benefitting Hyperliquid’s revenue model (accelerating token buybacks) and by extension its token price, and is a large part of the reason for its outperformance in recent weeks (YtD performance HYPE +62 percent vs BTC -20 percent and ETH -29 percent).

The popularity of these markets has also seen Binance expand commodity exposure through Binance Wallet perps in early March, listing both WTI crude oil and natural gas contracts, with the exchange using Aster airdrop points as incentives to attract early volume to the new markets.

TradFi is capitalising on tokenised securities

While decentralised and centralised crypto exchanges start providing access to traditional assets through perpetual futures, traditional exchanges are moving towards tokenised securities, with 24/7 trading and near-instant settlement being a large, if not the most important, part of the appeal.

The SEC just last week approved Nasdaq’s proposal to allow certain securities to trade in tokenised form, with eligible participants able to opt to settle trades as blockchain-based tokens that trade alongside traditional shares on the same order book, at the same price and with identical rights and the same ticker. Settlement is run through a pilot by the Depository Trust Company (DTC).

Nasdaq has also partnered with Kraken, who will offer tokenised versions of Nasdaq-listed stocks to customers outside of the US (particularly in Europe). These tokenised shares will also function like regular equities, with holders able to vote on company decisions and receive dividends.

Intercontinental Exchange (ICE), the parent company of the NYSE, recently invested in crypto exchange OKX at a reported USD 25B valuation, and OKX users will soon be able to trade NYSE-listed tokenised stocks and derivatives.

Regulatory clarity edging closer

The SEC’s approval of Nasdaq’s tokenised securities pilot is encouraging, however, a full rollout is not expected until early next year as regulation is still being finalised and blockchain rails still need to prove they can support the weight of regulated securities at scale.

What a tokenholder actually owns and whether those rights would hold up in court are cross-jurisdictional questions between US, European and Asian regulators that need to be worked through, and admittedly, institutional capital is unlikely to flow into these markets until they are.

Commodities like gold and oil carry far less regulatory baggage than equities, which is a large part of why volumes on platforms like Hyperliquid have grown as quickly as they have.

Outlook

The harmonisation efforts between the SEC and CFTC are very encouraging signs, with the two agencies recently signing a memorandum of understanding (MoU) to coordinate joint oversight over crypto and tokenised assets.

We expect TradFi to continue its push to bring capital markets on-chain, but this will be gradual, and for now it is the likes of Hyperliquid that are already capturing the demand. And with most altcoins trading heavily as a proxy to Bitcoin’s price action and market liquidity still very thin, crypto users may continue to rotate into traditional assets if they continue to generate better risk-adjusted returns.

A broader risk-on shift would require clear signs of de-escalation in the Middle East and the reopening of the Hormuz Strait, but as unfortunate as the situation is, the current geopolitical and macro backdrop is exactly what is accelerating tokenised RWA adoption from both TradFi and crypto markets.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.