Previous crypto market cycles have followed a predictable pattern, with Bitcoin leading in early bull cycles, and altcoins taking over later in the cycle. The current market cycle has failed to follow this pattern due to changes in market structure and a lack of user traction for most crypto use cases. The recent drop in Bitcoin’s dominance suggests that the long-awaited altseason may have arrived.

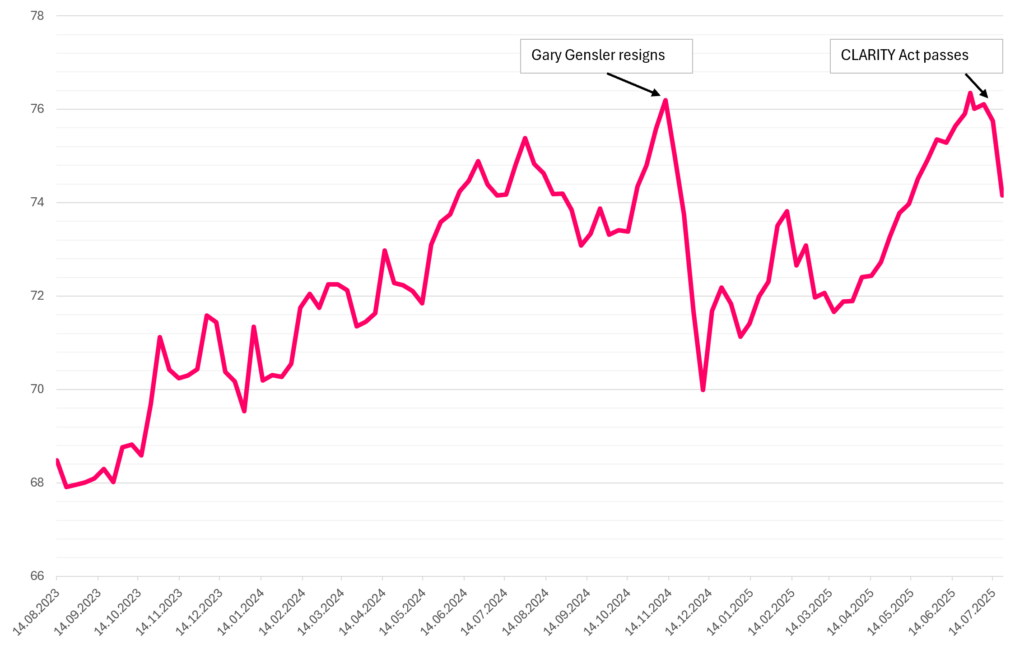

Bitcoin+Ether+Solana dominance

Source: CoinMarketCap

Since BlackRock filed to launch Bitcoin spot ETFs in the summer of 2023, the crypto market has been largely driven by institutional interest that primarily focused on Bitcoin and more recently extended to Ethereum and Solana.

This has led to a sustained step rise in Bitcoin dominance from below 40 percent to around 65 percent. This trend reversed sharply on Gary Gensler’s resignation last autumn, which gave justified hope that regulatory obstacles that have held the alt sector back will be removed. However, this proved to be a short-lived move as the market’s pessimism on real user traction for most of the sectors and use cases prevailed.

The recent steep drop in Bitcoin’s dominance reignited hopes that the long-awaited altseason may be finally under way. The move was in part due to the renewed optimism around Ethereum (and other major Layer 1s) as the stablecoin and tokenisation use cases were advancing, further supported by pro-crypto legislation, regulation and focus by major traditional financial institutions. However, as the combined dominance of the three majors also dropped, there are signs of the beginnings of a broader alt rally.

Is it altseason now?

Indices are still far from indicating an altseason, and the initial move towards altcoins (outside the three majors) was already partially reversed. This suggests that the market is still on the fence and hesitant to commit to use cases beyond projects that show strong revenue growth – which are few and far between (the best example currently being HyperLiquid).

Traditional investors that recently entered the crypto market have been quick to diversify, first extending their investment to the Ethereum ETFs in recognition of it being the likely main beneficiary of the stablecoin and tokenisation trends, and then beyond Bitcoin and Ether. However, this diversification mostly benefited crypto-related equities, such as the recently launched Circle or Galaxy, rather than altcoins.

Most of the new money that has entered the crypto market in the last 1.5 years is limited to investing in traditional wrappers such as ETFs or crypto-linked equities. As crypto acquisition vehicles are being launched on an expanding list of tokens beyond Bitcoin, this does bring incremental demand to the rest of the crypto market, but it remains to be seen if this will be sufficient to catalyse a true altseason.

Additionally, retail investor participation in the current bull cycle has remained low. This time, the source of the Bitcoin rally is not retail – a shift from previous cycles dominated by retail behaviour. This is also underscored by Google Trends data showing that search interest in ‘Bitcoin’ remains subdued compared to previous bull runs. As previous altseasons were strongly driven by retail investor exuberance, their continued reticence may limit the upside from an altseason.

On the other hand, retail investors may feel that they no longer have an edge to compete with institutions in the major tokens but may re-enter the crypto market when they see indications of an altseason. There are already signs pointing in this direction, for example, Google Trends for “altcoins” have picked up strongly in the last couple of weeks.

Retail investor behaviour aside, there are a number of drivers are in place currently that are likely to deliver an altseason – albeit a muted one.

Liquidity

Global liquidity is high and rising. Liquidity has been a key driver of financial assets since the 2008 crisis – in many ways keeping a broken system on life support.

More recently, plentiful liquidity has allowed risk assets to rally even in the face of negative macro developments and mounting risks.

As liquidity searches investable opportunities, this is likely to benefit the altsector of the crypto market – especially as most tokens have a relatively small market capitalisation.

Metrics such as the Fed’s National Financial Conditions Index, or global M2 show continued liquidity growth. The weak dollar contributes as most countries have significant dollar denominated debt, and slowing global growth is compelling governments and central banks to provide liquidity injections via fiscal and monetary means. Oil prices are also muted and, barring severe geopolitical shocks driving the oil price much higher, contribute to easy liquidity.

Revenue growth

At the same time, crypto investors have become jaded about the prospects for user growth and revenue generation for most crypto use cases after excitement in previous bull cycles repeatedly led to disappointment.

On the one hand, it is encouraging that the market has become much more discriminating – rewarding the rare instances of genuine traction while being much more wary of hype than during past cycles. On the other hand, this limits the prospects for the altseason, as very few crypto projects currently earn any significant amount of revenue.

Regulation

What can change sentiment, as well as protocol fundamentals over time, is the increasing regulatory clarity. Most significantly, the passing of the crypto market structure bill through Congress, and the likelihood of it progressing to being signed into law in the coming months is creating the foundations for crypto projects to build, innovate, and offer strong tokenomic models without the fear of litigation or regulatory penalties. This is further supported by the sharp pivot at the SEC under its new leadership, not only removing threats but proactively seeking to support the industry with clarity and feasible paths to compliance.

This can lead to real traction for use cases, and as projects generate meaningful revenues, it also allows them to directly link the token value to the profits. Not only does this make the tokens less speculative and more attractive to an increasingly sophisticated investor base, but it also makes the crypto asset class more investable for traditional financial institutions.

Barring such fundamental developments, liquidity may still suffice to catalyse an altseason, however, it may be then more focused on hype and market segments that lack fundamental value such as memecoins.

Summary

Rotation into altcoins from Bitcoin has been a mark of past crypto bull cycles, and it has been widely anticipated in the current cycle. However, Bitcoin’s unusually strong drivers and changes in market structure, with traditional financial institutions playing a far greater role, have delayed the altseason and are likely to keep it much more muted than in past cycles.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.