As US stablecoin legislation is making progress, it has fuelled widespread expectations of explosive growth in the use of stablecoins in payments and settlement. This was also underscored by the enthusiastic reception of the Circle IPO and the stock’s consequent stellar performance, as well as the similarly well received “pre ICO” of the stablecoin focused Plasma protocol. However, the market may overestimate the size of the stablecoin opportunity or the speed with which it may be realised.

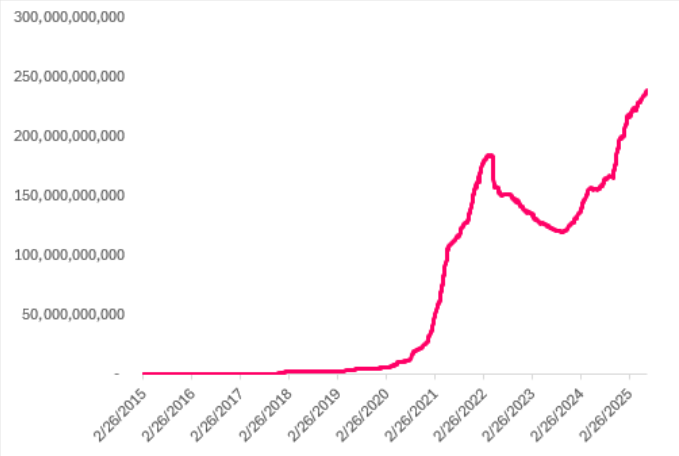

Stablecoin market capitalisation

Legislative progress in the US, investment by a host of large banks, payment providers, and retailers in stablecoin infrastructure, and repeated statements by the US administration that they see an important role for stablecoins has created a lot of excitement around this use case. Circle’s share price increased tenfold after the recent IPO and continues to trade 7x higher. Bullish narratives abound about the potential size of the market, with trillions of dollars expected in market capitalisation.

The stablecoin market capitalisation has been steadily growing over the past year and a half, and it is currently at an all-time high of USD 250bn. Meanwhile, US stablecoin legislation has cleared the Senate and there is a good chance that Congress might also pass the act as soon as this week, and it can then be signed into law.

The political will in support of stablecoins is strong as they are seen as a helpful source of demand for treasuries as government debt escalates bringing more supply – when demand is limited by the escalating fiscal deficit, the credit downgrade of the US, and the loss of faith leading to foreign selling of US assets. Stablecoins are also seen as a potential tool to reverse de-dollarisation.

Stablecoin use in payments is indeed growing, however, with a lot of great expectations and bullish predictions, where will the expected exponential future growth come from?

What are stablecoins used for?

Stablecoins were conceived as a convenient tool to facilitate crypto trading without having to use the high-friction process of fiat/crypto conversion. Their primary use case to this day is in crypto trading, and historically an increase in stablecoin market capitalisation has been a bullish sign for the crypto market, suggesting inflows into the asset class.

The parallel trend of tokenisation raises the prospect of fully on-chain financial markets where most assets could exist and operate entirely on-chain, interacting seamlessly across decentralised platforms with interoperable protocols allowing assets to be used across multiple applications (e.g., as collateral, in liquidity pools, or for governance). A meaningful shift towards these emerging “internet capital markets” would also create substantially more demand for stablecoins – however, this trend remains in its early stages.

Although stablecoin transaction volume has surpassed the combined volume of Visa and Mastercard, the comparison isn’t exactly fair as only a small portion of the stablecoin transaction volume is in real world payments – a fraction of the payments volume Visa and MasterCard process.

The growth in stablecoin use in payments is gradual rather than exponential, and the question is whether the trend will accelerate and what factors will drive it.

Settlements

Stablecoins are expected to play a transformative role in backend financial settlements due to their ability to provide instant, low cost, 24/7 transactions.

However, the expected growth of stablecoins in backend settlements is likely to occur primarily on private blockchains or permissioned networks. Financial institutions need to comply with KYC/AML, data privacy, and reporting requirements. Additionally, enterprises prefer environments where they can govern transaction rules, manage upgrades, and ensure uptime. Projects like JPM Coin, Partior, and Fnality are examples of stablecoin-like instruments used for interbank settlements on private networks. These systems are designed for high value/high trust environments, not open public access. Additionally, private blockchains can be more easily integrated with existing financial infrastructure.

Even with projects such as the JPMorgan deposit token pilot launched on Ethereum based Layer 2 Base, it is highly probable that JPMorgan will use off-chain netting and internal ledgering, and only settle net balances on Base. As Base doesn’t have a token, the only benefit to the crypto market is through the fees Base pays to Ethereum when it posts batches of transactions, with Base earning the majority of the fees paid by users.

It is unlikely that public stablecoins would be used in settlements, or that much fee revenue would be generated for crypto projects with a token.

Emerging markets and remittances

This is a very strong use case for stablecoins. In many emerging economies, people want to hold dollars to protect against inflation or currency devaluation. Stablecoins offer dollar access without needing a US bank account. Additionally traditional remittance services charge high fees and take days to settle. Stablecoins enable near instant, low-cost transfers across borders, often for a fraction of the cost.

Stablecoin use in emerging markets has been growing steadily for some time, with Tether commanding the vast majority of market share. There is no reason to expect that US stablecoin legislation would

change user behaviour in emerging markets, or that it would catalyse accelerated growth. The growth trends are expected to continue but this is a gradual rather than an exponential trend.

Adoption would, however, accelerate if US stablecoin issuers offered incentives – airdropping stablecoins, offering a yield, cashback, or other perks or benefits. Such benefits are already being offered by local fintech projects in some countries, by certain payment cards, and PayPal.

Cross border payments

The use of stablecoins in international trade is likely to rise over time as they offer faster, cheaper settlements, however, for most businesses to revamp their systems and operations is likely to take a long time.

There is a more immediate case for dollar stablecoins in trade involving businesses in emerging markets as they can access dollar liquidity via stablecoins without needing a US bank account. In countries with strict capital controls, stablecoins offer a workaround for accessing dollars in trade. However, governments may restrict or ban the use of stablecoins in trade due to concerns over capital flight or sanctions evasion, so this use case has limitations.

There are projects working on integrating stablecoins into trade finance platforms, enabling tokenised letters of credit, escrow, and invoice factoring, however, it will take some time before substantial volumes are executed.

Retail use in developed countries

This use case is the least likely to grow organically as there is little to no incentive for users to switch.

The backdrop of stable local currencies and efficient payment systems that often come with rewards, fraud protection, and consumer rights means there isn’t a pain point that stablecoins can address, while regulatory uncertainty, limited or no protection, stablecoin specific risks such as de-pegging or hacks, and in some countries negative tax implications provide deterrents.

It is unlikely that retail users in developed countries would switch to stablecoin payments without substantial and sustained incentives.

Summary

As stablecoin legislation is being enacted around the world and major banks, payment providers, and retailers are launching, or planning to launch their stablecoins, the expectations are very bullish for the growth of this market segment.

We expect to see increased use of stablecoins in payments, settlements, trade, remittances, as well as in the growing “internet capital markets”, however, we believe that the growth is likely to be slow and gradual, or implemented in a way that has only marginal benefits, if any, for public, investable crypto projects.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.