Decentralised lending was battle-tested in 2022, and it proved superior to centralised lenders. However, its product range is very narrow. Below, we examine the potential for decentralised lending to expand.

Eliminating the human element from lending decisions has significant potential benefits, such as trustless execution, faster transactions and reduced costs and fees. The value of the transparency provided by decentralised platforms has become more apparent recently, as reckless, negligent and sometimes fraudulent behaviour was revealed behind the opaque practices of several centralised lenders.

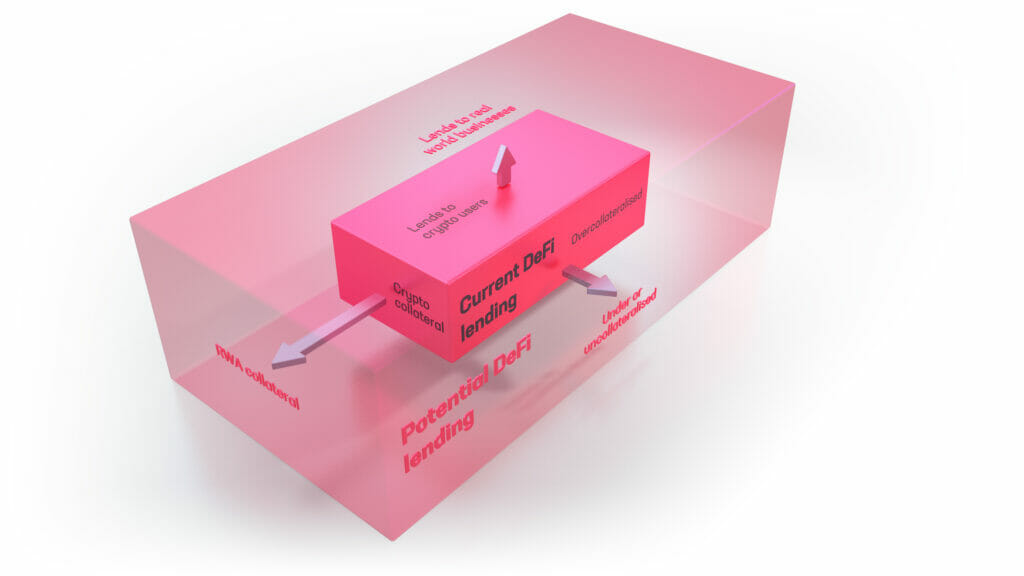

The practical challenges of providing credit in an automated fashion meant that, so far, DeFi lending has been mostly limited to overcollateralised lending against on-chain collateral. This also limited the borrowers to crypto traders and arbitrageurs. DeFi lending has provided a narrow offering to date.

However, the potential exists for decentralised lending to offer alternatives across most traditional credit sectors.

Undercollateralised or uncollateralised lending

Overcollateralised lending is not capital efficient, and therefore, the demand for it is limited. Overcoming this limitation requires undercollateralised or uncollateralised lending protocols that preserve privacy but access reliable data on creditworthiness to determine the risk profile of borrowers.

For individual borrowers, this can be solved with secure digital identity protocols that include information on assets, income and repayment history. Zero-knowledge proof technology is enabling data storage and access while preserving privacy. For corporates, it requires reliable financial information. In all cases, reliable oracles are required to deliver real-world information to the blockchain.

To date, uncollateralised lending protocols have relied primarily on centralised underwriters, with lenders contributing funds on the basis of their trust in the credit analysis. The short track records of these underwriters and the limited opportunity for diversification made the offering overly risky at this early stage. The total value locked (TVL) in these protocols reached a peak in 2021 with an aggregated estimate of close to USD 1 billion, but it declined during the bear market and crypto credit crunch to the current level of USD 50 million.

Nonetheless, there are a number of projects supporting the development of uncollateralised crypto lending, such as Credora (providing credit scoring services to lending protocols), Spectral Finance (developing on-chain credit scores) or DECO (focusing on privacy-preserving oracle technologies). These lending protocols are also experimenting with various risk management techniques: requiring pool underwriters to provide first loss capital, building in reserves, or a network of credit auditors, whose performance is monitored and incentivised on chain.

Challenges:

- Decentralised access to credit information to determine the debt ceiling and loan pricing, and to monitor creditworthiness during the life of the loan

- Active credit markets and improved on-chain risk management techniques

- Managing the recovery in case of a default

The most prominent protocols include Maple Finance, TrueFi and Clearpool.

Lending against real-world collateral

Another extension of DeFi lending is accepting real world assets as collateral. These assets could include receivables, real estate, consumer goods, royalties or loans.

Some projects, such as Centrifuge, tokenize real-world assets (RWAs), issue non-fungible tokens (NFTs) against them and create a marketplace for them on-chain. Other protocols, such as Goldfinch, do not tokenize the collateral asset, but they enter into legal agreements with the provider of the RWA collateral. MakerDAO has issued loans backed by RWA collateral such as tokenized real estate, tokenized freight invoices, trade receivables and loans.

To manage the risks on the valuation of the collateral and its limited liquidity, the loans that are backed by these assets often have senior and junior (first loss) tranches.

Challenges:

- Valuing the collateral and monitoring changes in its value

- Legal and regulatory risks to enforceability of the RWA contract, and the risk of double taxation with income-bearing collateral such as bonds

- Monetising the collateral in case of default

The most prominent protocols include Centrifuge, Goldfinch and MakerDAO.

Lending to real-world businesses or to individuals

Expanding the potential DeFi lending client base can be a source of market growth and risk diversification.

The loan may be collateralised with RWA assets or be uncollateralised and approved based on credit research or credit scores.

In either case, the loan needs to match the currency of the RWA collateral or the borrower’s revenues or income that the credit assessment is based on. In most cases, this means issuing the loan in fiat-linked stablecoins. The borrowers will typically want to convert the loan into fiat currency.

MakerDAO has innovated by lending to commercial banks against their loan portfolios (USD 100 million to Huntingdon Valley Bank and USD 30 million to Société Générale). Goldfinch is lending to SMEs in emerging markets using RWA collateral.

WeTrust revived the centuries-old concept of lending circles and replicated it on the blockchain to create lending pools among trusted parties.

Challenges:

- Verifying the borrower’s identity, which requires a centralised access point or blockchain-based identity technology

- The unclear regulatory status of DeFi in key jurisdictions, which poses risks when DeFi lending interacts with real-world businesses and individuals

- Managing the recovery process in case of a default

The most prominent protocols are MakerDAO, Goldfinch and WeTrust.

Further considerations

DeFi lending has extremely low duration currently, which makes it comparable to money markets. These possible extensions of DeFi lending change the risk profile by introducing much longer duration. This is especially so with lending to real-world borrowers, which is heavily weighted towards fixed rates rather than the variable rates that currently dominate DeFi lending.

As active credit markets develop on DeFi platforms, arbitrage opportunities will be created between TradFi and DeFi versions of the same products.

Interacting with real-world entities and real-world data introduces points of centralisation, including access points for censorship. Decentralised oracles, blockchain-based identity with zero-knowledge proof technology and blockchain-based credit scores are building solutions for this.

For DeFi lending to grow, the liquidity provision to these pools also needs to grow. A lot of that growth will need to come from non-crypto-native investors. For now, this tends to be channelled via CeFi gateways, such as crypto banks and asset managers.

Summary

The opportunity from extending DeFi lending to provide capital-efficient loans and compete with traditional finance on cost, speed, transparency and efficiency is significant. It is also a necessary step to prevent DeFi from remaining a marginal niche. There are still numerous practical challenges when implementing these extensions to DeFi, with a large number of projects working on offering innovative solution

To be the first to get the latest news on Sygnum and the market, expert insights and industry research please follow us on Linkedin and Twitter.

About Sygnum

Sygnum is the world’s first digital asset bank, and a digital asset specialist with global reach. With Sygnum Bank AG’s Swiss banking licence, as well as Sygnum Pte Ltd’s capital markets services (CMS) licence in Singapore, Sygnum empowers institutional and private qualified investors, corporates, banks, and other financial institutions to invest in the digital asset economy with complete trust. Sygnum operates an independently controlled, scalable, and future-proof regulated banking platform. Our interdisciplinary team of banking, investment, and Distributed Ledger Technology (DLT) experts is shaping the development of a trusted digital asset ecosystem. The company is founded on Swiss and Singapore heritage and operates globally. To learn more about Sygnum, please visit www.sygnum.com.

Disclaimer

This information was prepared by Sygnum Bank AG. This information may contain forward looking statements and may be subject to change. The opinions expressed herein are those of Sygnum Bank AG, its affilitates, and partners at the time of writing. This is for informational purposes only and contains general material. It does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum Bank AG to purchase or sell assets or securities. It is not intended to be used as a general guide to investing, and it should be used for informational purposes only. When making an investment decision, you should either conduct your own research and analysis or seek advice from an expert to make a calculated decision. The information and analysis contained here have been compiled from sources believed to be reliable. However, Sygnum Bank AG makes no representation as to its reliability or completeness and disclaims all liability for losses arising from the use of this information.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.