Although Bitcoin has made a new all-time high in mid-March, indications are that there is potential for significant continued performance in the current bull cycle.

Considering a combination of typical crypto market cycle behaviour, signals of cycle stages and the fundamental drivers in place, we expect the current bull market to continue for some time and deliver substantial returns between now and the cycle high.

The pattern of past cycles

We define a bull cycle as a phase during which the market makes a new all-time high. We determine the top of the cycle once the market drop that follows exceeds one standard deviation. The up and down cycles are pinpointed from the low to the high and from the high to the low.

Duration of Bitcoin up and down cycles in years

So far each bull phase in the crypto market lasted 2-3 years, followed by steep declines of around 85% on average lasting about a year. The current bull cycle started 1.3 years ago (with the cycle bottom at the end of 2022), and based on past patterns, it is expected to last another 1-1.5 years.

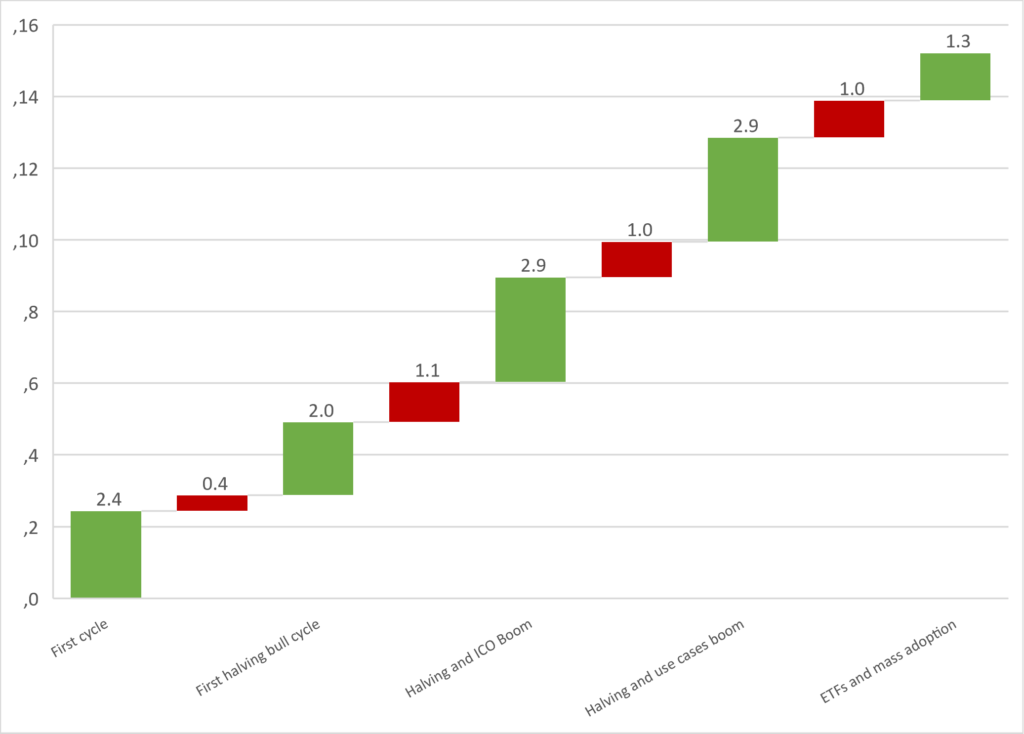

In terms of performance, bull cycles have delivered extraordinary returns. The early cycles had extremely high % returns, starting from a low base (over 56,000% price appreciation for Bitcoin during the first halving bull cycle). The bull market fuelled by the 2016-17 ICO boom generated close to a 12,000% return, while during the last bull cycle when use cases started to proliferate, Bitcoin rose 2,056% and the overall market rose 2,213% (S&P Broad Crypto Market Index).

So far Bitcoin is up 294% from the cycle bottom (363% to the new high before the correction), and the overall market is up 249% (315% to the high). Although cycle returns have been declining from the initially astronomical levels, even extrapolating the trajectory of lower cycle highs suggests at least an additional 50% performance – which may well be exceeded due to the specific fundamental drivers in place in the current cycle.

In past cycles, a new all-time high was reached roughly two-thirds of the way through the bull phase. In this cycle, Bitcoin making a new all-time high already might suggest that cycle returns will be greater than the extrapolated trajectory would suggest. Meanwhile, the overall market is still 15% below its previous all-time high, and past patterns would imply that a new all-time high will be reached around the end of the year. Should this happen sooner, it would underscore the likelihood of higher cycle returns.

Signals of cycle stages

The early stage of bull cycles is characterised by a lack of conviction, low volumes and tentative market moves. Although the cycle will have bottomed, the market environment still feels bearish and “wintery”. This phase lasted until autumn 2023.

When bullish sentiment takes hold and volumes accelerate, this is initially driven by market insiders – hedge funds, traders, and institutions already active in the market. Market participation broadens mid-cycle, while late-cycle behaviour is characterised by aggressive retail buying and a spike in the share of short-term holders.

Bitcoin has led each bull cycle, with the rally broadening around mid-cycle. Bitcoin’s dominance typically declines in the latter phases of the cycle, with the rest of the market outperforming Bitcoin. As recent cycles were characterised by a broadening of use cases and real-world applications, the overall market ended up outperforming Bitcoin over the full cycle. Bitcoin’s dominance increased during past bull markets until the later phases of the cycle, when it sharply declined.

The current indications are that we are still in mid-cycle. The rest of the market is still underperforming Bitcoin substantially (by 45% since the cycle bottom).

Bitcoin’s dominance has increased from 38% at the cycle bottom to 52% and remains at those levels without any signs yet of the typical later-stage decline in dominance.

Retail engagement remains moderate so far. A good proxy for this has been searches for the terms crypto and Bitcoin on Google trends, which remain at levels far from previous cycle highs.

Meanwhile, the share of long-term holders is still close to all-time highs, and there is no sign of the sharp uptick in short-term holdings that is indicative of the late stage of a bull cycle.

Fundamental factors

While fitting past patterns gives us some indication, as market psychology has a certain consistency, and the various indicators of market stages are fairly reliable signals, ultimately, fundamental factors can trump the above. A shock event with market-wide implications can terminate a bull cycle, while unusually strong fundamental drivers can extend the cycle, both in duration and in terms of the cycle highs it can reach.

After the recent launch of Bitcoin ETFs in the US by some of the world’s largest traditional financial institutions, demand for these products is steadily ramping up and this is likely to continue for some time. The existing inflows have already caused demand shocks in the crypto market, but most platforms have yet to approve the product, and some of those that have approved it report seeing only a very small percentage of early adopters engaging with the new products at this point. Meanwhile, countries around the world are introducing regulatory changes that allow greater engagement with these or similar products or are authorising the launch of such products in their jurisdictions.

The credentialing and legitimising effect of the approval of the Bitcoin ETFs and the involvement of leading traditional institutions has also kickstarted formal allocations to the asset class by asset managers. This trend is still in a very early stage, but we have seen a number of announcements of institutions creating an asset allocation bucket in their portfolios for crypto or starting due diligence. With a global asset management industry with assets under management of USD 120 trillion, the opportunity for further demand shocks is significant.

Inflows into Bitcoin are also supported by its increasingly widespread acceptance as a safe haven alternative to precious metals, and the growing demand for safe haven assets, in general, is based on the escalating macroeconomic and geopolitical instability around the world. After the upcoming halving late in April 2024, Bitcoin’s stock-to-flow ratio will be vastly superior to that of gold, making it the “hardest” asset.

Meanwhile, supply scarcity and the lack of selling by long-term holders means that inflows into the asset class have a strong multiplier effect. We have observed recently that a USD 1 billion net inflow into the Bitcoin ETFs on 12 March raised Bitcoin’s market capitalisation by almost USD 100 billion – a multiplier of 100x.

Risks

Unforeseen “black swan” events can shortcut bull cycles such as the Mt Gox hack suddenly ending the first crypto market bull cycle. That aside, the greatest risk currently is the ongoing push by the SEC to classify the majority of crypto assets as securities. Although judgements and comments by presiding judges in the relevant court cases have been leaning in crypto’s favour over the past 6-9 months, there is no final resolution yet. The market’s current optimism on the outcome means that negative developments could be detrimental to market sentiment, and serious negative developments on the regulatory front could cut the bull cycle short.

Summary

Fitting the pattern of past cycles to the current market conditions and observing the indicators that can pinpoint how far along we are in the current cycle all suggest that the current bull market has a lot further to go. When combining this with the fundamental drivers in place, the expectation is that the current bull cycle could surprise to the upside in terms of its duration and returns to the cycle high.

Read more about crypto assets from Sygnum here.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.