Cryptocurrencies, like Bitcoin, are more than just a new form of money. They are redefining our financial ecosystem and the way we perceive the role of traditional intermediaries. At the same time, they provide an opportunity for financial empowerment to the masses.

What sets them apart from traditional currencies, like the dollar or euro, is their multi-dimensional properties. They are not only a form of payment, but also a technology, a store of value, and an alternative financial market infrastructure. It is no wonder why they have disrupted the status quo, and why there are complications when trying to box crypto into existing classification frameworks. They are unlike any other asset we know.

In this article, we will explore the widespread adoption of crypto as a means of payment and how this particular feature is shaping up to be one of the most influential megatrends in future finance.

So, what is a “means of payment” exactly?

It refers to a payment method that allows individuals and businesses to transfer funds and settle transactions. It is a means through which buyers and sellers exchange value for goods and services. Typically, this has been in the form of banknotes, cards, cheques, credit transfers, direct debits, and so forth. But these payment methods rely on centralised intermediaries, like banks and financial institutions, to facilitate the exchange.

Bitcoin was inherently designed for payments

Bitcoin was initially designed as an alternative payment system by empowering users with the freedom to transact directly between one another (peer-to-peer or P2P), providing a new level of financial autonomy and privacy, away from banks.

When used as form of payment, Bitcoin (the cryptocurrency) is the payment instrument, which uses the Bitcoin network (the payment rail) to facilitate an exchange between a buyer and seller. As a currency, Bitcoin can also serve as a unit of account.

A unit of account refers to the property of an instrument that serves as a standard measure for comparing the value of goods and services. It allows us to assess the worth of artworks, cars, houses, and other goods by using a specific form of currency, whether it be fiat, cryptocurrencies or other financial instruments.

Bitcoin allows users to assess the value of money and establish a common denomination or unit of measurement. For example, by comparing a car priced at BTC 1 and a motorcycle at BTC 0.25, we can easily compare their relative prices. Bitcoin’s divisibility (up to 8 decimal places) and fungibility (each Bitcoin holds the same value as another) make it suitable for serving as such.

Over time, however, this alternative payment system has morphed into an entire industry of its own. This is due to the underlying technology, blockchain, which has opened up endless possibilities for industries with centralisation concerns to be dismantled and replaced with decentralised, P2P-driven use cases.

Despite market uncertainty, Bitcoin’s activity continues to increase year-on-year.

Source: Sygnum Bank insights, Dune

Yet despite its evolution, the fundamental purpose of Bitcoin remains the same – enabling secure, trustless transactions without the need for intermediaries, anytime and anywhere.

The unique and decentralised transactional qualities of blockchain networks, like Bitcoin and Ethereum, and the fact that each blockchain has its own native currency (the payment instrument), have allowed these networks to gain widespread acceptance as legitimate payment rails for exchanging goods and services.

Similar to traditional payment rails, like PayPal or an automated clearing house (ACH), a blockchain network serves as the backbone infrastructure that allows the cryptocurrency transfers to be made between senders and recipients. But the key difference lies in its decentralised architecture – meaning it is not controlled by a single operator.

Crypto payments offer several advantages compared to conventional payment methods:

- Low transaction fees

- Near-instant settlement

- Borderless transactions

- No chargebacks

- Avoid intermediary and currency conversion costs

- A new and growing customer base

- Advanced cryptography used to safeguard transactions

- Cryptocurrencies can function as a unit of account

Innovations and developments accelerate crypto payment opportunities

As encouragingly, to match the growing demand of cryptocurrencies, innovations like Layer 2 (L2) solutions (to optimise scalability), stablecoins (to manage volatility), as well as merchant solutions and mobile payment applications (to improve usability) have flourished, providing users and businesses with the opportunity to accept and use crypto as a means of payment.

Even countries, where inflation is high or a large proportion of their population are unbanked or underbanked, or where traditional financial systems are deemed unreliable, have witnessed a surge in crypto payments, thanks to these innovations.

The sheer number of over 420 million global crypto owners alone makes it evident that the crypto industry is anything but speculative, but rather a thriving and rapidly evolving industry.

The current state of crypto payments

The emergence of new market sectors like stablecoins, DeFi, NFT marketplaces and GameFi has resulted in the creation of new merchant segments. Not only has this created new demand and business opportunities, but also it has led to the formation of specialised crypto payment companies and products, like BitPay, Circle, Coingate, Ramp, Coinbase, Kraken, and Ripple, among others who provide the crypto payment gateways.

Thanks to the increasing regulatory clarity in some jurisdictions, crypto payments are also breaking into traditional market sectors, like e-commerce (for online purchasing), the gig economy (for contract and freelance workers), remittances (for sending money back to your origin country), travel (for bookings and reservations) and online gaming (for in-game item exchange), to name a few.

To date, there are more than 15,000 businesses that accept crypto payments around the world.

To match the rising demand from customers, leading payment giants like Mastercard, Visa, PayPal, Stripe and Venmo have all partnered with crypto companies, providing millions of users with access to crypto as a means of payment. Most major retailers like Overstock, Microsoft, Expedia and Starbucks have also integrated crypto payments, allowing their customers to directly purchase digital and physical goods with cryptocurrencies. Other major companies include the popular streaming company Twitch, Norwegian AIR, Etsy and Burger King.

El Salvador and the Central African Republic have taken a step further and recognised Bitcoin as legal tender, further increasing the adoption rate of crypto for general household payments. Crypto payment processors like Ibex Pay and OpenNode have now been able to on-board major fast-food chains and local businesses. Countries like Venezuela, Columbia and South Korea have also witnessed an increase in the number of retail and food and beverage businesses accepting crypto payments.

Crypto’s ability to promote financial inclusion and significantly reduce the cost of remittances are also showing notable signs of development. The remittance market, which is currently valued at almost USD 1 trillion is plagued with high cost-bearing traditional payments methods, charging workers up to 8 percent of the total transaction value. Crypto-friendly remittance services like Strike’s Send Globally, which leverages Bitcoin’s Lightning Network, offers a significantly cheaper alternative, ranging from 0.01 to 0.1 percent of the transaction value. Roughly 500 million people have access to Send Globally.

With almost USD 800 million in remittances sent home by migrant workers in 2022, crypto-based remittances could save the industry anywhere between USD 40 to 64 billion in costs per year.

So how can we monitor the growth of crypto-based payments?

The biggest concern when monitoring a blockchain’s network activity is that it does not present a precise picture of crypto-based payments. This is because all transactions are recorded on a blockchain, so it may be difficult to filter out which transactions have been specifically used for payment-purposes only – like cross-border money transfers or online purchases. Plus, most of the volume happening on a blockchain network is attributed to trade-related activity (to and from exchanges, verifying transactions, etc.) while smaller transactions (less than 100, 50, 20 USD) can also be facilitated by bots. While possible, it is still a laborious process, but there are a few general approaches to consider:

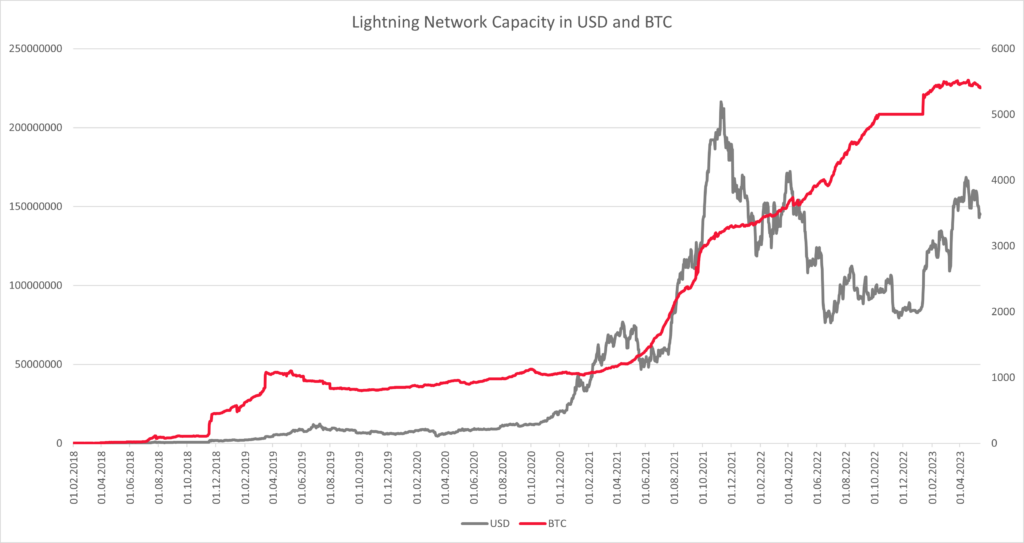

Lightning Network

Source: Sygnum Bank insights

One method is through the Lightning Network, a Layer 2 (L2) payment protocol that enables near-instant payments and reduces network congestion on the Bitcoin blockchain. Since its inception, it has shown impressive growth, as demonstrated in the graph below.

Growth of Lightning Network’s capacity. Source: Bitcoin Visuals The adoption of the Lightning Network has been steadily increasing in emerging markets like Africa and South America, primarily due to the efforts of Strike’s mobile application and remittance service. However, its overall growth has been due to a growing list of payment companies, like Strike, Cash App, Paxful, among others, that are expanding into various countries across the world. Another example is El Salvador’s national Chivo Wallet, which enables Lightning Network transfers thanks to infrastructure providers like River Financial who is responsible for powering the payment gateway. As a result, Lightning Network transaction volumes saw a major uptick over the course of last year. Today, there are over 18,000 active lighting nodes and 74,000 active payment channels running on the network, with over 5,230 BTC locked (capacity) in these nodes worth approximately USD 155 million. 666 merchants already use the Lightning Network, a 20 percent increase since the start of the year, and a 50 percent increase since early 2022. As Bitcoin transaction fees experienced a surge in price due to Ordinal inscriptions (Bitcoin NFTs), users in Africa are turning to the Lightning Network (and stablecoins), which may further accelerate its usage for crypto related payments in the coming weeks and months. While these figures are promising, the Lightning Network is just one aspect of the evolving world of crypto payments.

Stablecoins

Another way to track crypto payments is through stablecoins, which offer an alternative to volatile cryptocurrencies. The reason for their popularity lies in their fixed prices, with most stablecoins pegged to a fiat currency, like the dollar. Since the launch of Tether (UST), many stablecoins have entered the market with various token models and assets backing them.

Although stablecoins are primarily used to facilitate on- and off-ramps for crypto exchange users, they have gained increasing popularity for cross-border transactions and other forms of on-chain settlements. This is because they utilise blockchain networks and therefore offer a low-cost, secure, and competitive payment option compared to conventional means. This is also why regulated entities like Xapo Bank have recently decided to integrate stablecoin payment rails, using USDT and USDC for retail customers, as an alternative to slow and expensive SWIFT transactions.

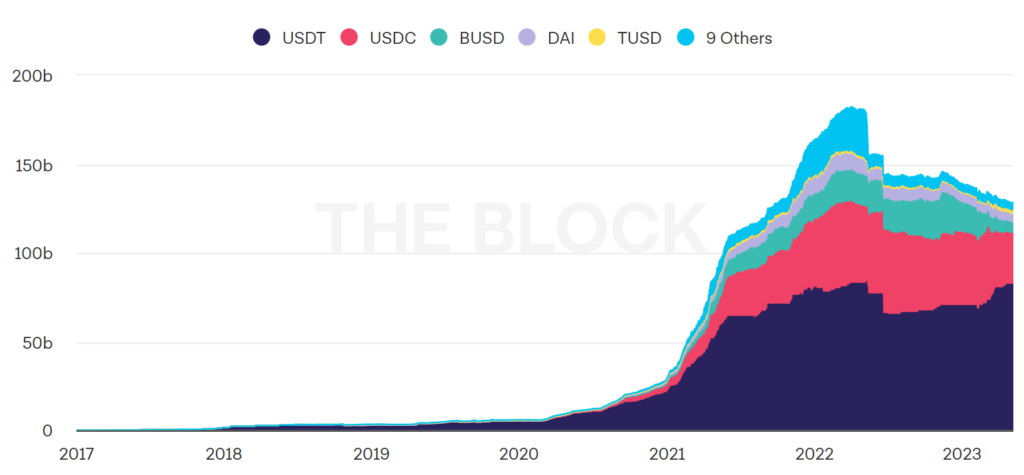

Stablecoin market capitalisation

Source: The Block

The growth of the stablecoin market can be seen in its remarkable rise in market capitalisation, with Tether regaining a significant portion of the market share as a result of the recent banking crisis.

Despite the majority of stablecoin volumes being primarily associated with crypto trading, monitoring this growth can still provide valuable insights into the increasing demand for crypto-based payments – especially now as more payment applications, merchant solutions and businesses begin accepting them as an official payment instrument.

Companies enabling crypto payments

Although this method is more of an estimate and less data-driven, tracking the growing number of companies accepting crypto payments can provide meaningful insights into the overall reach of customers who have the option to use them. While it may be difficult to filter out the exact percentage of crypto-based payment transactions (without requesting third-party data from the companies themselves), the growing list of retailers, payment service providers, and businesses accepting crypto is a strong indication that more and more users are demanding crypto to be used as a means of payment.

According to a 2022 report by PYNMTS and BitPay, who surveyed over 2330 merchants with a minimum of USD 250mn in annual online sales, around 85 percent of big retailers (who earn more than USD 1bn per annum) currently offer crypto as a payment method. Almost half of all merchants surveyed accept crypto and among the merchants that do not, 42 percent plan to do so.

The report also found that the majority of merchants use non-crypto native wallets to enable crypto payments, like PayPal and Venmo. Hence, it would be invaluable to conduct further research on these companies – more specifically, what percentage of their total payment volumes are crypto-based only.

A great example is global payments processor Checkout.com, which launched its 24/7 stablecoin settlement solution last summer, enabling merchants to process crypto payments from their customers. Following the successful pilot phase and launch that saw Checkout.com settling over USD 1 billion in crypto merchant transactions, they are now optimising their solution to onboard more merchants and offer a wider range of crypto assets.

Overcoming barriers to crypto payment adoption

Accepting crypto as a means of payment still faces several challenges, with price volatility being the primary one. For instance, a business or shop owner may fear having less in their account if the crypto market experiences a downturn and crypto prices decline. However, for the time being, this can be quickly remedied with crypto-to-fiat or stablecoin conversions, although this may result in additional costs.

Regulatory barriers also remain a major challenge, with many governments and institutions remaining sceptical or even threatened by cryptocurrencies. Some jurisdictions have embraced crypto-based payments with clear classifications for payment use cases (i.e., Switzerland’s payment token, or El Salvador accepting Bitcoin as legal tender). The EU is also working towards a framework which include “e-money tokens“, while others have responded by seeking to implement their own privately issued currencies, like central bank digital currencies (CBDCs). However, the latter approach defeats the very purpose of blockchain technology, and removes the benefits of security, decentralisation and transparency. To put it bluntly, issuing CBDCs do not even make use of blockchain at all.

Yes, regulation is necessary for guiding new forms of decentralised money, especially with regards to AML/CFT regulations. But perhaps a more lenient approach towards “controlling” the technology itself may be necessary, while ensuring that companies (especially centralised finance or CeFi entities) using crypto payments adhere to regulatory obligations.

Another challenge is the risk associated with fiat-backed stablecoins. These stablecoins rely on third-party custodians, like a bank. This dependency can pose a risk to the stability of the stablecoin if the custodian bank collapses, as seen with Silicon Valley Bank and the immediate impact it had on various stablecoins, like USDC. This issue may be remedied with algorithmic or decentralised stablecoins, however algorithmic models also present a risk due to the volatile nature of the cryptocurrencies backing them.

Despite the challenges, decentralised networks have proven to be very effective as robust payment rails used by millions of users and businesses worldwide. And, as the industry matures, the market will also likely converge around a few dominant currencies for payment purposes only.

Crypto as a means of payment will flourish in the long-term

So where does this leave us?

The evolution of blockchain technology on a mass scale is inevitable, which means cryptocurrencies will follow suit.

As payment services, merchants and users increasingly adopt crypto as a means of payment, cryptocurrencies are gaining recognition as a serious alternative to legal tender – in fact, in some cases, they have even become as such.

We know that blockchain works, that networks are reliable infrastructures, and that cryptocurrencies are effective payment instruments with clear benefits over traditional methods. This is why we continue to see year-on-year growth in the rate of adoption, irrespective of price fluctuations and regulatory barriers.

That being said, crypto and blockchain’s ability to unlock the full potential of digital payments should not be underestimated.

END

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.