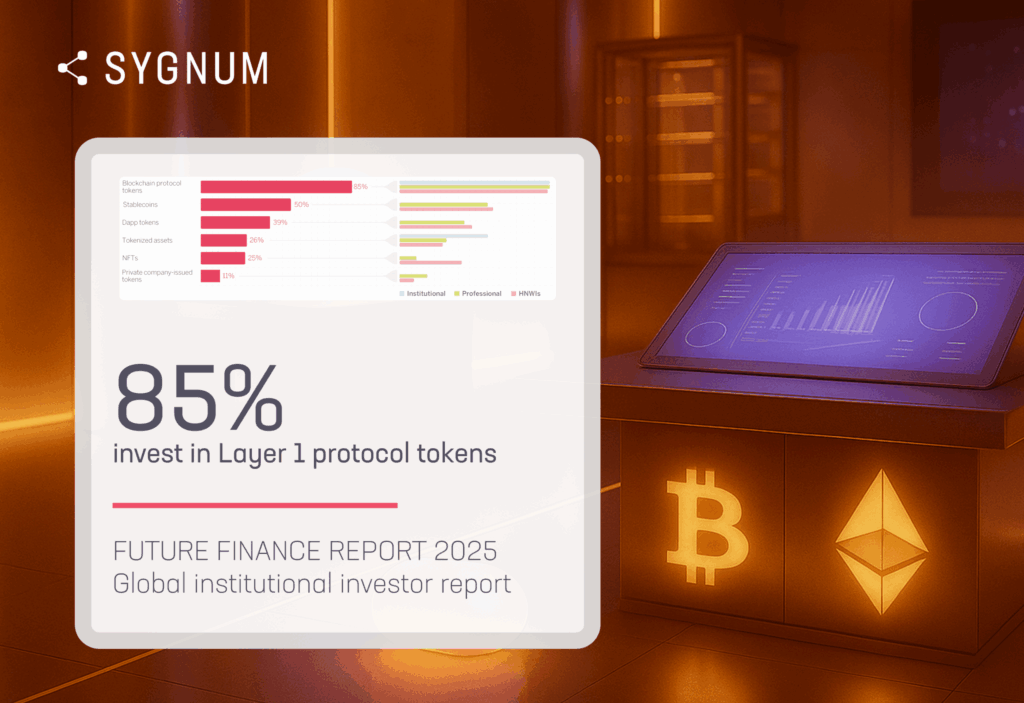

Sygnum’s Future Finance Report 2025 shows strong support for Bitcoin in a reserve role, with 81 percent of respondents agreeing it can be considered a viable reserve asset. Download the full report to get the complete story.

Demand for Bitcoin continued to be supported by its perceived safe haven qualities. As state and local governments advance proposals for Bitcoin reserves, this has the potential to translate into direct demand while further cementing its role as a store of value asset.

This also leads the price of Bitcoin to be influenced by macro trends that inspire growing demand for safe haven assets overall – such as mounting sovereign debt reaching unpayable levels or heightened geopolitical risks.

On the back of this, Bitcoin as a treasury reserve asset has developed into a major theme but has been met with both progress and pushback throughout the year. Several US states have passed their own Bitcoin reserve bills, while others have rejected or vetoed them. The US Bitcoin Act, which would establish a federal stockpile still remains far from certain, while Switzerland, Japan, Germany and Brazil are showing progress.

However, adoption is largely dominated by Michael Saylor’s Strategy approach, which turned its treasury into a leveraged acquisition vehicle. The approach has been widely imitated by other small-cap companies but widely contrasts with the more cautious approach of corporate treasures, whose mandate is to protect the financial stability of company assets. This may explain why interest in Bitcoin as a treasury reserve asset is growing, but has not yet been adopted more widely by large corporate treasurers.

Nonetheless, the survey shows strong support for Bitcoin in a reserve role, with 81 percent of respondents agreeing it can be considered a viable reserve asset. The 19 percent that are either hesitant or disagree aligns with the reality that corporate treasurers are tasked first and foremost with safeguarding the balance sheet and financial stability of the company – even as Bitcoin gains wider recognition as a store of value. At the same time, caution is also tied to concentration risks due to the fact that Strategy now controls more than 3 percent of the total Bitcoin supply. Perhaps this is why shareholders from major tech companies like Microsoft, Meta (formally Facebook) and Amazon have publicly rejected reserve allocations.

When asked about the opportunity cost of holding cash instead of Bitcoin over the next five years, 71 percent agreed that cash would carry the greater risk. Disagreement was higher here, with 10 percent firmly opposed and 20 percent neutral, suggesting greater caution at this point in the cycle.

Ethereum is now firmly appearing in corporate treasuries, with public companies collectively holding more than 6 million ETH, equivalent to 5 percent of the total circulating supply, while corporate allocations are now extending to Solana and BNB. However, these follow the same leveraged acquisition playbooks pioneered by Strategy.

Meanwhile, central banks have been quiet on the subject, but any re-emergence would be a powerful demand catalyst for Bitcoin and the broader crypto market. Deutsche Bank recently suggested that Bitcoin could one day join gold on central bank balance sheets, but the prospect remains speculative at best. Nonetheless, the topic has entered mainstream financial debates, which shows how far the conversation has already moved.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.