Market sentiment improved notably as Ethereum celebrated its 10th birthday this year. After a difficult period of readjustment, there is a tangible feeling of optimism that the world’s leading smart contract platform is now facing a brighter future.

The price of its native token, Ether (ETH), has risen rapidly in recent months, breaking all-time highs in August, and turning the tables on Bitcoin with a markedly better relative price performance. This has raised hopes that ETH can post a sustainable bounce-back to lead the long-awaited altseason.

Ethereum vs Bitcoin vs Solana performance (%)

Source: CoinMarketCap (since Pectra upgrade)

What factors contributed to this? The Prague + Electra (Pectra) upgrades have gone a long way to solving technical difficulties within the ecosystem. ETH staking has been given fresh impetus both by the Pectra upgrade raising the staking cap (from 32 to 2048 ETH) and the SEC’s clarification on protocol staking activities, raising the odds that staking could be included in Ethereum ETF products this year.

This has been accompanied by a spate of crypto-friendly US legislation that bodes well for clearer classification rules, as well as more stablecoin activity and tokenised securities launches on the Ethereum blockchain.

Demand for Ether has also been boosted by record inflows into Ethereum ETFs and a fresh catalyst in the form of corporate treasury purchases, copying the Bitcoin acquisition vehicle strategy.

These tailwinds have led to a sharp drawdown in ETH reserves on crypto exchanges. So could a continuation of rising demand for ETH culminate in another supply crunch and upward price shock?

Ethereum’s turnaround

Ethereum looks to have turned the corner and finally cleared the headwinds that had been giving the ecosystem such a turbulent ride over the last 18 months. Only a year ago, Ethereum was going through a mid-life crisis, with the price of Ether languishing compared to Bitcoin and the whole ecosystem struggling to keep pace with a flood of memecoins.

Transaction bottlenecks and high gas fees were accompanied by a shift in fee revenue from Ethereum’s Layer 1 to Layer 2 projects that were siphoning activity away from the base layer. This was especially (and still is) the case with Coinbase’s Layer 2 Base, which dominates Layer 2 activity while operating without an investable token.

Fees paid to Ethereum’s base layer fell by 80 percent since Q2, leaving revenue optics weak at time when other tokens were rallying and Bitcoin’s demand drivers kept Ethereum out of the spotlight.

The smooth execution of the Pectra upgrade added staking improvements and more blob capacity, building on the scalability gains from Dencun that had already cut Layer 2 fees substantially. However, the lowering of fees for Layer 2s has been mirrored by a decline in Ethereum’s deflationary fee-burn rate schedule (which is analogous to a share buy-back program), resulting in a mild inflationary environment for ETH issuance.

But with a fresh revamp of its development roadmap, the Ethereum Foundation and several Layer 2 rollup companies publicly displayed a strong, coordinated effort to unify its ecosystem and bring more settlement activity back to the base chain.

This is expected to be corrected (or at least partly) by the upcoming Fusaka upgrade, which will expand Ethereum’s data availability and make it more attractive for Layer 2 rollups to post larger data loads directly on Ethereum instead of using external DA (data availability) layers.

ETH demand surges to all-time high

Meanwhile, there are more powerful tailwinds driving Ethereum’s positive outlook, and demand for ETH has returned to the market after a quiet couple of years. In August ETH reached new all-time highs of USD 4,945, the first time it has broken previous price records since November 2021.

Last year’s limp ETH price performance compared to Bitcoin has quickly reversed. The price of ETH has risen around 140 percent since the Pectra upgrade compared to 15 percent for Bitcoin and 42 percent for Solana.

The SEC gave Ethereum another regulatory boost by clarifying that “protocol staking activities” do not constitute as security offerings under federal law. Not only will the integration of staking clearly differentiate Ethereum ETFs from their Bitcoin counterparts, but it will also act as a catalyst for fresh institutional flows looking to benefit from the passive staking yield.

The optimism has already translated into strong flows, and by early September US spot Ethereum ETFs had attracted USD 10.75 billion in net inflows since the start of the year. Ethereum ETFs dominated throughout August, with daily inflows hitting record highs, while concurrent Bitcoin outflows point to a potential rotation of institutional capital.

ETH price gains have driven total assets under management to an all-time high of USD 27 billion, up more than 150 percent this year.

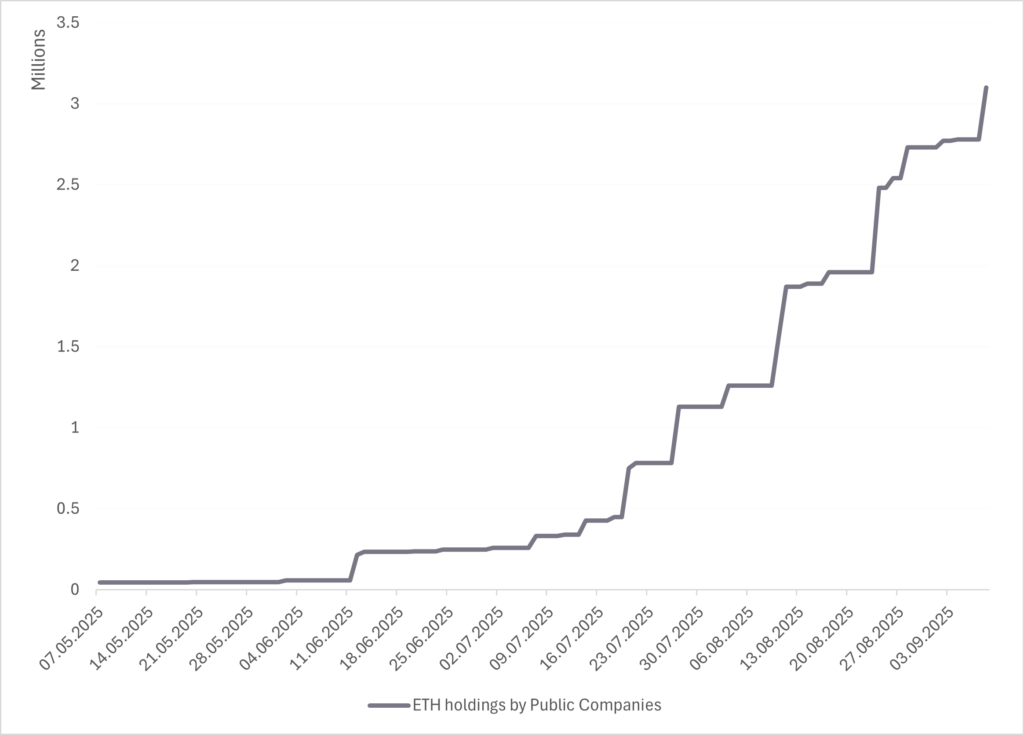

New source of ETH demand

After the heavy stockpiling of Bitcoin by Strategy and other companies, ETH has now emerged as the new favourite cryptocurrency for corporate treasuries. With Bitcoin demand cooling, attention is shifting to the yield opportunities that Ethereum can provide.

BitMine has established the largest ETH treasury with holdings above 2 million ETH and continues to expand its position through ongoing purchases. Meanwhile, Sharplink plans a USD 1 billion ETH allocation while Bit Digital has fully shifted its treasury from Bitcoin to Ethereum. Gamesquare, BTCS and Ether Machine are also raising capital to launch their own ETH treasuries. Public company holdings now exceed USD 13 billion in ETH.

ETH holdings by Public Companies (ETH cumulative)

Source: The Block

Because ETH is a yield-bearing asset via staking rewards or DeFi protocols, companies can generate income by holding ETH rather than simply stockpiling as a passive store of value.

But the new trend of companies pivoting their business models into crypto stockpiling has raised some concerns, particularly models like Strategy that rely on the underlying volatility between the price of the cryptocurrency and their own share price, or with small-cap stocks overshooting after announcing their crypto treasury pivots (as seen with the recent 30x surge in Eightco (OCTO).

Therefore, regardless of the substantial purchases from companies, this emerging trend should be viewed with some caution.

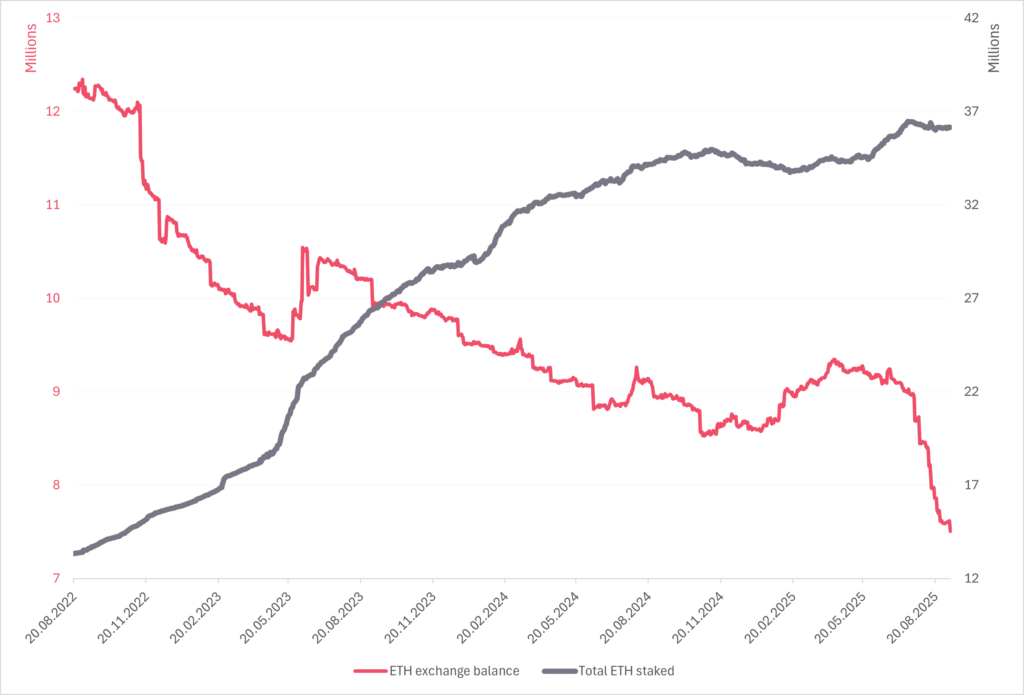

Looming supply shock?

As demand for Ethereum builds up from multiple sources, there is a clear trend of its liquid supply shrinking. ETF inflows, whales accumulating large amounts of ETH and corporate acquisition vehicles are withdrawing reserves held on exchanges at a considerable rate – which have now broken below cycle lows (and are still shrinking).

Meanwhile, the exit of ETH from crypto exchanges has also been matched by an upsurge in staking deployment on a longer timeframe, with nearly 30 percent of ETH’s liquid supply now currently locked in various DeFi platforms, staking and restaking protocols.

Deposits are likely to continue as the odds of approving ETF staking (with in-kind redemptions recently approved) grow increasingly more favourable.

Spot Ether exchange balances vs total ETH staked (in ETH)

Source: CryptoQuant

Other positive drivers

The passing of the GENIUS and CLARITY acts in the US Congress in July (with GENIUS signed into law) have also contributed to the positive momentum, with Rep. French Hill recently noting that the CLARITY Act could pass within weeks given its overwhelming bipartisan support. The legislation marks a significant step forward in the regulation of crypto assets, providing both legal certainty around stablecoins and resolving ambiguity over which crypto assets will be classified as securities or commodities.

This will open the door for more institutional offerings, an area where Ethereum already dominates in both stablecoins and tokenisation activity. Société Générale’s SG Forge is launching a dollar stablecoin on Ethereum with BNY Mellon as the custodian, while Citigroup is exploring its own tokenised deposit products.

The GENIUS Act may also bring Bank of America into the market, who specifically named Ethereum as the key settlement rail for regulated stablecoin activity.

Meanwhile, traditional companies like Shopify have partnered with Coinbase and Stripe on a stablecoin payment system. Stripe has built its own USDC payments product, and Visa is working with Bridge to develop credit cards for stablecoins.

Ethereum and TRON are the primary stablecoin rails with approximately 80-85 percent combined market share, but this may soon be tested by the upcoming stablecoin-focused network Plasma Chain by Tether. Solana and other high-performance blockchains are also competing aggressively to capture the next wave of stablecoin activity.

However, the impact will fall more heavily on TRON, which carries most of Tether’s volumes and relies on the leading stablecoin for most of its revenues, while regulated stablecoin flows such as USDC continue to expand on Ethereum.

Ethereum’s stablecoin market capitalisation has risen to nearly USD 150 billion from USD 104 billion a year ago. The market for tokenised securities has also mushroomed to USD 8.3 billion.

Entry vs exit staking queue misconception

There are some concerns that the recent rise in Ethereum’s staking exit queue signals looming sell pressure, but the reasons are in fact technical.

The backlog is largely a result of trades where ETH is staked and more ETH is borrowed against liquid staking tokens, which were also staked (often in multiple loops), and became unprofitable once ETH borrowing rates moved above staking yields.

These loops started to unwind when ETH borrow rates on platforms like Aave touched 6.64 percent in July, sending validators into the exit queue to free collateral.

The surge in exits was therefore the consequence of higher funding costs, not investors cashing out. Borrowing costs climbed because demand for leverage was increasing, and while those positions needed to be rebalanced, it was not a “bearish” signal at all.

At the same time, the staking entry queue climbed to new all-time highs and has since flipped above exits, showing that fears of a potential sell-off were unsubstantiated.

Outlook

Ethereum can look forward to its next birthday with less trepidation than a year ago, as it looks to have shrugged off many of the most pressing issues that had been contributing to its longstanding underperformance.

The Ethereum blockchain will likely remain the de facto choice for both DeFi innovation and institutional adoption for the foreseeable future and gives Ethereum a great advantage in capturing a large part of the anticipated rise in stablecoin issuance and institutional adoption trends.

There is also strong evidence that a growing number of traditional investors and firms are looking at ETH as a mainstream asset and are prepared to divert capital flows in the cryptocurrency via ETFs and corporate acquisition vehicles.

Against the backdrop of liquid ETH exchanges reserves below cycle lows and demand from ETFs and acquisition vehicles accelerating, Ethereum now faces a very real prospect of a supply squeeze that will certainly test the market.

ENDS

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.