This year, the tokenisation of real-world assets (RWA) is one of the most promising trends in crypto. The benefits range from tokenised illiquid assets to new and improved secondary markets and a potential DeFi ecosystem fully powered by stable, reliable collateral. Could tokenising RWAs finally bridge the gap between the crypto and traditional worlds?

The breakout of decentralised finance (DeFi) and Non-Fungible tokens (NFTs) may have overshadowed tokenisation’s slow start, but given its complexity and the far-reaching ramifications it has for financial markets and regulators across a range of assets, it is no surprise that it will take time to gain traction.

Initially in the form of security token offerings (STOs) back in 2018, these tokenisation efforts were limited to fundraising and mostly executed on private chains, which, coupled with regulatory implications contributed to the hype’s quick demise.

But in recent years, however, the tides have turned, and institutions have begun to explore tokenisation with a broader range of assets such as bonds, equities, fixed income, and real estate with more success.

Institutions are beginning to understand DeFi’s resilience

The string of centralised finance (CeFi) bankruptcies also demonstrated the effectiveness of DeFi. Protocols underwent heavy stress testing through several mass liquidations and crypto selloffs, yet they remained fully operational. This has led to even greater confidence in the underlying protocols and the emergence of several institutional-led tokenisation initiatives using DeFi.

In recent months, institutions like ABN AMRO and Siemens, among others, issued digital bonds for the first time on public blockchains. Global investment manager Hamilton Lane tokenised its private equity fund using the Polygon blockchain. DeFi protocols like MakerDAO opened a real-world asset (RWA) collateral vault for Societe Generale and Ondo Finance launched a tokenised fund based on US Treasuries and corporate bonds.

These are just a few examples, but it is quite impressive to witness traditional institutions placing their trust in trustless protocols and using them as powerful tools for bringing RWAs on-chain. Not too long ago, many in the traditional community considered this a non-option.

But what does it really mean to tokenise RWAs?

Tokenisation is simply the process of converting the ownership rights of physical or financial assets into digital tokens. They are essentially digital replicas that offer an immutable and transferable unit of ownership. These tokens can then be issued, bought, sold and traded across a variety of exchanges and networks.

There are various assets that can benefit from tokenisation: Regulated financial instruments like equities, bonds, funds and loans, along with tangible assets like gold, real estate, artworks or other precious metals can all benefit from tokenisation. By enabling fractional ownership, tokenisation could lower investment thresholds for things like real estate. For asset managers, tokenisation may open up new distribution possibilities for their investment funds.

The advantages of tokenising RWAs are extensive: They include benefits like 24/7 on-chain trading, faster settlement, injecting liquidity into previously inaccessible or near-absent liquid markets, automating compliance, and creating new forms of credit and investment opportunities. With tokenisation, assets that were once off-limits can now become new financial products and even rival with traditional ones. For instance, tokenised real estate could eventually compete with real estate investment trusts (REITs) since they are more accessible, require less investment capital and offer higher yields.

That said, it is no surprise that 97 percent of institutional investors believe that tokenisation will revolutionise asset management and 91 percent want to invest in tokenised products, as reported in an October 2022 BNY Mellon survey.

Even some experts predict that tokenisation for global illiquid assets could become a USD 16-68 trillion market by 2030. Such a number is not unrealistic given that the fixed income debt market alone is worth an estimated USD 127 trillion, global real estate USD 362 trillion and gold USD 12 trillion in market capitalisation.

Institutions continue to successfully tokenise RWAs

Many mainstream institutions have realised this potential. Singapore Central Bank’s Project Guardian successfully used DeFi for wholesale funding markets, where JP Morgan, DBS Bank and SBI Digital Asset Holdings executed trials for foreign exchange transactions and government bond trades using public lending protocol Aave and decentralised exchange (DEX) Uniswap. Siemens issued a EUR 60 million digital bond on the Polygon public blockchain, cutting out the need for paper-based global certificates and central clearing. Deutsche Bank began testing tokenised funds on the Ethereum public network.

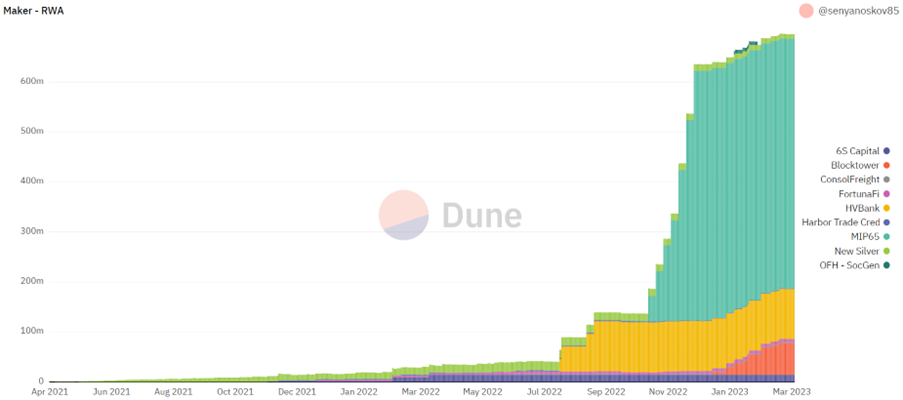

Even DeFi entities have been busy with MakerDAO leading the way with USD 680 million worth of RWAs backing its stablecoin DAI. Other protocols like Ondo Finance launched tokenised ETFs backed by US treasuries and corporate bonds, while Centrifuge and Goldfinch are tokenising RWAs to provide credit, proving how DeFi lending has extended its reach into accepting RWAs as collateral.

Last week, real-estate company Homebase listed its first real-estate backed NFT on the Solana public blockchain, allowing customers to fractionally invest in tokenised real estate. The tokens are issued via an STO and are registered as securities with the SEC.

RWAs on private blockchains

Of course, there are also numerous tokenisation initiatives on private chains, but they have purposely been left out in this article. While they are a step in the right direction (and dependent on use case), they remain siloed and limited – even more so in their potential to address trust concerns, tampering and bad business practices.

Yes, traditional institutions favour private initiatives given that trust has a very different meaning to the typical crypto-native user. Their trust requirements demand well-established, even perhaps flawless, guardrails before they consider deploying trillions of dollars worth of assets on just a few lines of code.

But times are changing, and public protocols are becoming increasingly relevant for financial institutions. For instance, they can leverage them via privacy preserving layers (like zero-knowledge proofs) to maintain their identity and discretion over asset transfers. Of course, there are also numerous tokenisation initiatives on private chains, but they have purposely been left out in this article. While they are a step in the right direction (and dependent on use case), they remain siloed and limited – even more so in their potential to address trust concerns, tampering and bad business practices.

Barriers to adoption

There are, however, a few challenges to adoption, with the biggest ones being a lack of perceived urgency and regulatory clarity.

As mentioned above, the benefits are clear, but without widespread demand and readily available products for institutions, there is little incentive for them to engage or launch their own initiatives at competitive rates – at least for now.

This is also due to the absence of strong regulatory frameworks, which creates legal uncertainty for tokenised assets and other issues regarding roles and processes in the asset value chain. Plus, there are general scalability issues with blockchains as they would need to manage traditional finance (TradFi) market volumes.

DeFi and TradFi, a collegial relationship

Still, to truly drive efficiencies and accessibility of RWAs on a larger scale, both traditional and DeFi markets need one another:

Traditional entities require robust protocols they can trust and DeFi needs traditional entities to co-create safeguards and bring RWAs on-chain. It is a collegial relationship that can boost institutional trust and adoption, and help DeFi expand its product offering, lending capabilities and collateral options.

All this remains to be seen, of course. But tokenising RWAs may just be the key to achieving real-world adoption, bringing serious capital and liquidity into a volatile yet fully capable crypto ecosystem.

It is just a matter of time.

Learn more about digital asset banking at Sygnum here.

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.