In this excerpt of Sygnum’s research report Valuing crypto assets, we explore methodologies and other factors driving the accurate valuation of cryptocurrencies.

This article is part of Sygnum’s Valuing crypto assets investment research report.

Commonly used valuation techniques

There have been several various methodologies proposed, but many of these give only limited and incomplete insight into the fundamental value of cryptocurrencies.

Many of these techniques are useful and provide important pointers, but on their own, they do not constitute comprehensive valuation models.

We discuss several of these methodologies below, focusing only on models for fundamental valuation. In this report, we do not cover any sentiment indicators or trading signals such the MVRV ratio (market value versus realised value).

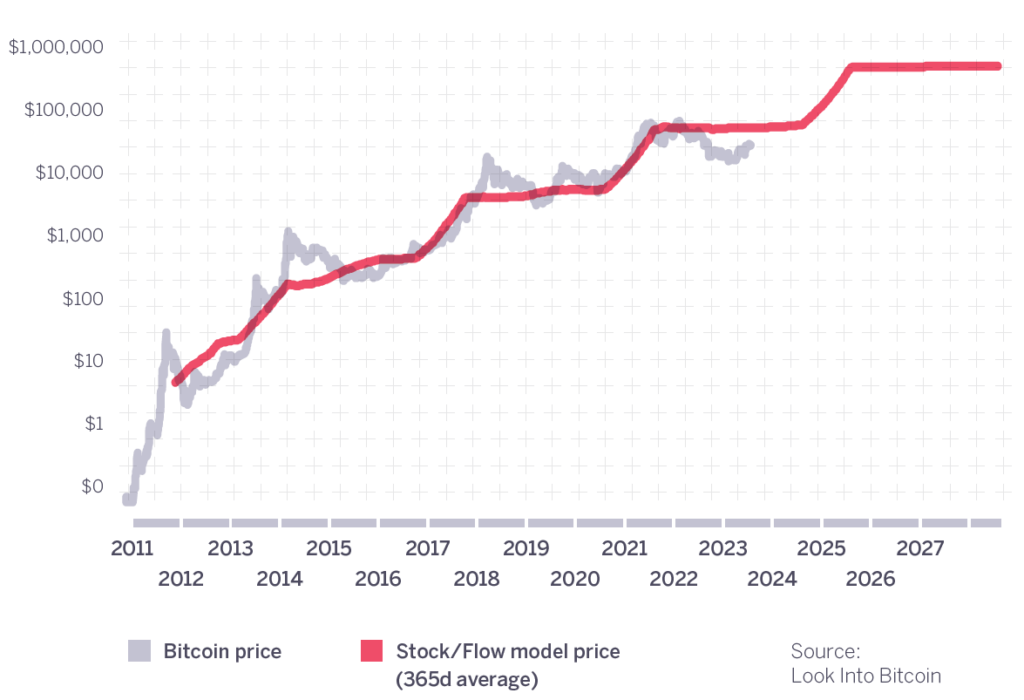

Stock-to-flow

A valuation technique borrowed from the commodities market, it assesses the relative scarcity of an asset by comparing its existing stock (supply) to newly created supply (flow).

BITCOIN STOCK-TO-FLOW RATIO

But unlike commodities, whose demand is largely predictable, ignoring the demand side when valuing Bitcoin is not a reasonable valuation methodology. Indeed, valuing cryptocurrencies involves assessing the fair market capitalisation, and the token supply is used merely to translate this into a fair price per token. The supply in itself does not drive the fair market capitalisation.

And while scarcity is a necessary requirement for a good store of value, scarcity itself is not valuable. There are many things that are in very scarce supply that no one wants and therefore they have no value. A change in the rate of supply growth (e.g. Bitcoin halving) may have an impact on sentiment, but it does not in itself increase the value. If demand stays constant, a slower rate of supply growth is still growth, i.e. it is still dilutive rather than value enhancing.

The fact that cryptocurrencies’ supply models are transparent and well-known also means that there is no positive or negative surprise, except when there is a change to the monetary policy of the cryptocurrency (as was the case with Ethereum recently). Barring such a change, the supply side of the valuation is perfectly predictable.

Ultimately, assessing the value of cryptocurrencies lies in assessing future demand and value creation.

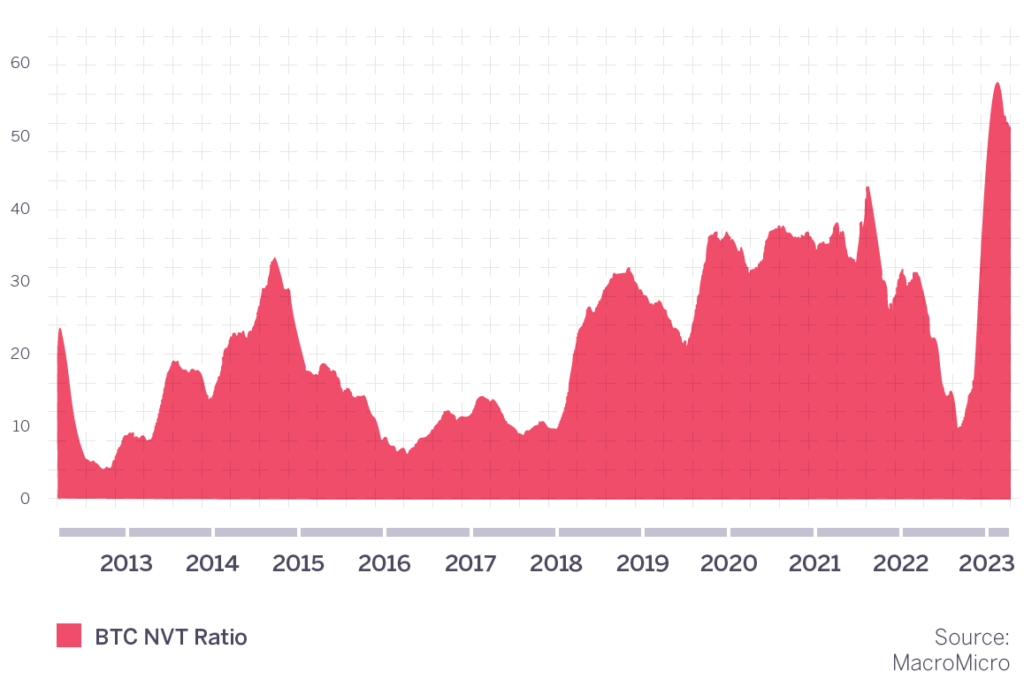

NVT (Network Value to Transactions)

The network value to transactions ratio (NTV) compares the market value of a cryptocurrency to the volume of transactions processed by the network.

The metric can highlight valuation anomalies across tokens or for the same token over time.

BITCOIN NVT RATIO

Its limitation is similar to that of the P/E ratio for stocks in that a high multiple can express either the market’s actual expectation of high future growth or overvaluation. As it is a combination of both, it is hard to disentangle.

It can, however, be used for reverse enquiry: is the growth implied by the NVT ratio higher or lower than the investor’s reasonable expectation?

It is also important to note that the NVT ratio only assesses a protocol’s value based on the volume of transactions it processes, and it ignores other growth drivers, such as the use of a cryptocurrency as a store of value.

In addition, to the extent that it assesses value based on the activity on the network, it is important to keep in mind that network activity translates into value very differently for Proof-of-Work vs Proof-of-Stake protocols, so their NVT ratios are not comparable.

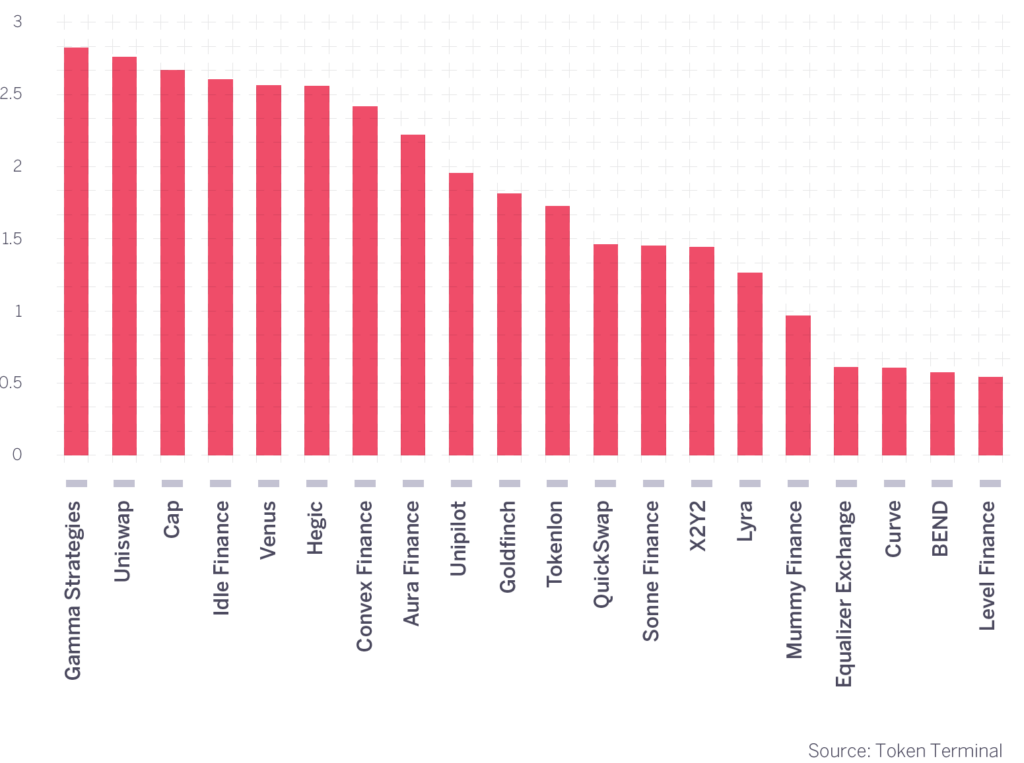

Fees, revenues or profits versus market capitalisation

There are other metrics that more precisely target the value that accrues to a protocol than the NVT ratio. Instead of using the transaction volume, similar ratios can be calculated by using the fees paid to the protocol, the revenues or the profits earned and comparing them to the token’s market capitalisation.

These metrics have a higher information content because a high volume of transactions at very low fees may generate less economic value than lower volume at higher fees, and ultimately, the token’s fundamental value is driven by the value it captures.

Revenues earned are even more precise, as they subtract any fees paid out by the protocol. For example, in the case of a decentralised finance platform, they subtract the fees the protocol pays to liquidity providers.

Profits of decentralised platforms are often close to platform revenues, as the cost of operating these platforms is typically very low. Some Proof-of-Work blockchains are an exception, however, there both the costs and the revenues accrue to the miners, and they affect the token’s value through a different mechanism.

PRICE-TO-FEES RATIO OF SELECT DEFI PROTOCOLS (AS OF 18/4/23)

These metrics are similar to P/S (Price-to-Sales) and P/E (Price-to-Equity) metrics for stocks and have the same limitations as those ratios. As in the case of the NVT ratio, they signal the market’s growth expectation, and they are useful for reverse enquiry, spotting outliers or tracking a token’s market valuation over time.

Network effects – Metcalfe’s Law

‘Metcalfe’s Law’ says that a network’s value is proportional to the square of the number of nodes in the network. It is an important insight for valuing blockchain protocols, as it highlights that the value of a network grows considerably faster than its user base.

Metcalfe’s Law tells us that forecast growth in user numbers translates into exponentially greater network activity. It also tells us that a protocol with a larger existing network will capture a disproportionate share of the total economic value available to the sector.

BITCOIN’S MARKET CAPITALISATION VERSUS METCALFE VALUE AT YEAR END 2009–2022

However, as a valuation metric, Metcalfe’s Law has its limitations, as it fails to consider how a protocol’s market share translates into value for the token. Proof-of-Work versus Proof-of-Stake protocols capture value differently. Some platforms have very low fees relative to others. Consequently, on its own, Metcalfe’s Law is simply a tool but not a valuation methodology.

Miners’ cost

Some have proposed that the cost of producing a cryptocurrency puts a floor under its valuation. This is no more true for cryptocurrencies than for any other product. If the market does not pay a price that is higher than the production cost, the latter needs to adjust or the company in question will go out of business. We saw this recently when Bitcoin miners’ costs exceeded their revenues. This did not lift the price of Bitcoin, nor did it give Bitcoin any ’value’, rather miners started going out of business.

Bitcoin has a built-in mechanism to adjust the cost of mining if the amount of hash power committed to the network falls. It does this through adjusting the ’difficulty’ which drives the amount of computing power required. So rather than providing a floor to the Bitcoin price, the marginal cost of production will adjust downwards. This will also make the network less valuable as its security levels decline as the number of miners falls.

Although the ’marginal cost of production’ is not a valuation methodology of any sort for cryptocurrencies, it is still an important metric to track as it provides information about fundamental trends for the protocol, including network security and potential selling pressure for the token.

BITCOIN AVERAGE MINING COSTS

Comparables

Although not a technique to assess the absolute value of a token, comparables provide useful pointers for the relative value of cryptocurrencies.

Various metrics such as the number of active users, connected wallets, unique visitors and so on can be tracked and compared across protocols and over time.

The caveats are that the same number of users may generate more economic value on one platform vs another and that the price of a token discounts the expectation for future growth rather than reflects the current level of activity. These comparables are nonetheless useful as they provide proof points on the project’s success over time and relative to other projects.

DAILY ACTIVE USERS OF SELECT LAYER 1 AND LAYER 2 PROTOCOLS (AS OF 18/4/23)

Measuring protocol quality

Although not valuation methodologies as such, metrics that measure a protocol’s quality across various metrics nonetheless provide useful insights that can be used to assess whether a platform has better or worse growth prospects.

For blockchain protocols, the qualities that certain metrics seek to measure relate to the level of decentralisation and the likelihood of attacks.

The Nakamoto coefficient measures decentralisation and represents the minimum number of nodes required to disrupt a blockchain’s network. A high Nakamoto coefficient implies greater security, making the network more valuable.

The Gini coefficient, originally used to measure income or wealth inequality in countries, is used to track the concentration of cryptocurrency holdings. Although higher concentration is considered a negative, it is important to understand the full context when comparing projects, such as the stage of maturity.

BITCOIN’S WEALTH DISTRIBUTION

The longevity of a protocol is also highly relevant as a proof point, and we need to take it into consideration when comparing younger projects to more established ones.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.

Disclaimer

This document is purely for educational purposes and has been issued by Sygnum Bank AG. It is not intended for distribution, publication, or use in any jurisdiction where such distribution, publication, or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a marketing communication. It does not constitute an offer or a recommendation to subscribe, purchase, sell or hold any security or financial instrument. It contains the opinions of Sygnum Bank AG, as at the date of issue. These opinions and the information contained herein do not take into account an individual‘s specific circumstances, objectives, or needs. No representation is made that any investment or strategy is suitable or appropriate to individual circumstances or that any investment or strategy constitutes personalised investment advice to any investor. Therefore, you must verify the above and all other information provided in the document or otherwise review it with your external advisors. Some investment products and services, including custody, may be subject to legal restrictions or may not be available worldwide on an unrestricted basis. The information and analysis contained herein are based on sources considered as reliable. Sygnum Bank AG uses its best efforts to ensure the timeliness, accuracy, and comprehensiveness of the information contained in this document. Nevertheless, all information indicated herein may change without notice.