The tokenisation of publicly listed stocks is one of the most talked about trends, as the demand to bring capital markets on-chain is gaining wider support among TradFi and regulators worldwide.

After BlackRock’s CEO Larry Fink urged the SEC to fast-track the tokenisation of stocks and bonds earlier this year, and SEC Chair Paul Atkins confirmed the US regulator will support tokenised securities, several exchanges moved quickly to bring their products to market.

Robinhood, Kraken, Bybit and Gemini (and soon eToro) have each launched tokenised access to US equities, although they vary in how the tokens are held and in how far they can interact with DeFi applications and blockchain protocols.

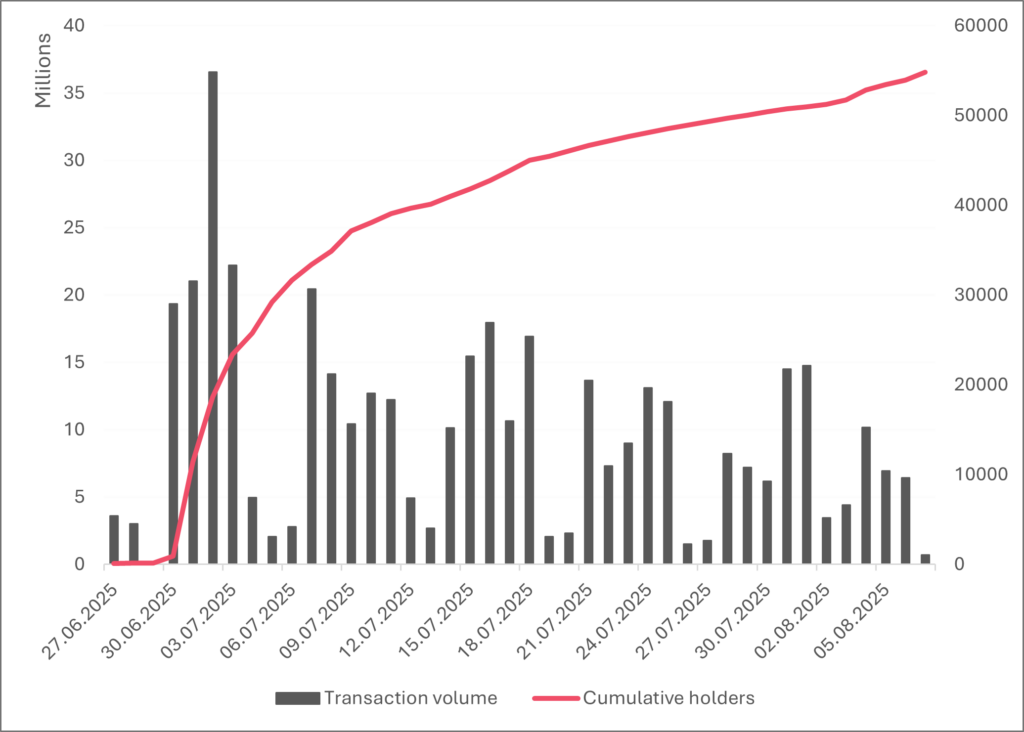

The trend took off quickly, with the tokenised equity market growing in value, as well as an increase in new issuances and tokenholders. However, traded volumes have begun to subside, and since the current offerings are primarily targeting retail and crypto investors, the anticipated institutional flows that would likely catalyse the next phase of growth are still missing.

xStocks daily transaction volume vs cumulative holders

Source: Dune

Nonetheless, it is an important first step, and the public support from leading TradFi institutions may soon push regulators and institutional-grade platforms to put in place the necessary infrastructure and safeguards needed for this transition to proceed. Some jurisdictions like Switzerland and Liechtenstein already have clear regimes for tokenised securities, and the EU is trialing tokenised shares under its DLT Pilot Regime (which ESMA recently reviewed). However, no jurisdiction currently supports a tokenised public equities market at scale.

Why tokenise stocks?

The whole point of tokenising stocks is to streamline access across the entire asset lifecycle, which means bringing these instruments closer to the speed and flexibility of crypto assets. By issuing stocks as on-chain assets (i.e. tokens), they become substantially more efficient by significantly reducing settlement times, costs and making them tradeable outside of the usual traditional trading hours.

Tokenised stocks operate on blockchain rails, so users can integrate them into DeFi applications for lending, yield strategies or other DeFi-related use cases. Depending on the product , some can be moved to crypto-native wallets and may even accrue dividends in stablecoins or other tokens.

But there are also trade-offs. For instance, tokenholders are not listed as shareholders, meaning they have no voting rights and do not have a direct claim on the underlying stock (this is a major blocker for institutional mandates that require enforceable ownership rights).

Current offerings on the market

Robinhood launched tokenised stocks on the Ethereum Layer 2 solution Arbitrum, with plans to launch its own proprietary blockchain by the end of the year. The popular exchange now offers over 200 stocks and ETF tokens to its European client base, including names like Apple, Microsoft, as well as OpenAI and SpaceX. Trades are commission-free and tradable 24 hours a day, five days a week.

However, if users want to access tokenised stocks, the tokens remain locked within the Robinhood platform. They cannot be transferred to external wallets or used in DeFi, and the underlying shares are held in SPVs managed by Robinhood (or its affiliates), and all trading activity is contained within a closed system.

Dividends are credited in euros but processed internally by Robinhood. This is because exposure to the underlying shares is synthetic and there are no direct entitlements from the actual company itself. Governance remains off the table and all corporate actions follow the platform’s internal processes.

Point being, these tokens only track price and carry none of the rights that come with legal share ownership.

Swiss-based tokenisation platform Backed Finance also launched its xStocks product, offering over 60 tokenised US stocks on Kraken, Bybit and a few Solana protocols. Kraken offers tokenised stocks under a Liechtenstein SPV with the underlying shares held in custody. Its model is different to Robinhood in the sense that the tokens are live on the Solana blockchain and can be transferred to personal wallets.

xStock token can therefore interact with protocols like Raydium and Kamino, where users can use them as collateral in liquidity pools and access new forms of on-chain yield. Trading is also available 24 hours a day, 5 days a week, with price feeds maintained through oracles and a mint-redeem mechanism.

Dividends are paid either through airdrops or by crediting holders with additional xStock tokens equal in value to the dividend. No fiat is actually paid, and, as with Robinhood, holders have no legal ownership or voting rights in the underlying shares – these rights remain with the custodian. Bybit offers an identical product to Kraken.

Gemini is the latest exchange to the enter the market, offering 37 US stocks via its partnership with the tokenisation platform Dinari. The tokens are issued as dShares on Arbitrum using Ethereum’s ERC-20 token standard. Users can hold fractional positions, trade in the same manner as Kraken and Bybit, while the underlying shares are held off-chain by a custodian. Dinari distributes the dividends in the form of USD+ or other stablecoins.

Challenges and misconceptions

As previously mentioned, these tokenised products do not offer shareholder status. Dividends, redemptions and corporate actions are all processed at the discretion of the platform or tokenisation service provider – not from the company itself. This also means that these tokens fall outside established investor protection regimes, so things like SIPC (Securities Investor Protection Corporation) do not apply.

They also carry no voting rights. This matters less in passive exposure like crypto ETFs but in direct equity holdings, it is a core element of ownership and for many institutional mandate is an absolute requirement.

Liquidity is another big issue; order books are still very thin and trading outside traditional market hours often leads to price dislocations that persist until primary markets open again. Arbitrage is also limited, as redemptions can only be processed when the underlying stocks are trading.

A user-friendly interface or “all-in-one” platform to trade stocks and crypto assets may be appealing for retail and crypto investors, but without clear disclosure around ownership rights, many users are likely to misinterpret tokenised exposure as equity ownership. Even OpenAI has publicly rejected Robinhood’s new OpenAI tokens, stating that they do not represent equity in the company and were issued without the company’s approval.

Hybrid models are likely the end state for institutional capital

For crypto investors, the ideal outcome would be fully native decentralised equities issued and traded entirely on-chain, but current legislation and the structure of capital markets make this unpracticable.

Corporate registries, shareholder and voting rights are heavily embedded into current statutory frameworks, and are unlikely to be made legally binding through smart contracts and replicated on public blockchains without changes to securities law.

This is why the likely end state is in the form of a hybrid model (public / permissioned), where tokenised equities benefit from the efficiency gains of using blockchains and DeFi applications, while anything legally enforceable continues to depend on traditional market infrastructure.

How would institutional capital flow into on-chain capital markets?

Stocks could be issued on a public blockchain like Ethereum or Solana, with smart contracts setting the transfer rules and managing their on-chain lifecycle. The underlying equity would still sit with the custodian or SPV, but a token standard like ERC-1400 (or similar) could, in theory, allow the custodian to pass voting rights, dividends and other corporate actions directly to verified wallets in a legally enforceable way. This could technically given tokenholders many of the same entitlements as direct equity ownership, even if their names never appear on the issuer’s share register.

ERC-20 tokens could be customised to do the same, but this would require a lot of custom controls and compliance layers, making it far more complex than using a standard that was purpose-built for traditional securities.

In this theoretical model, dividends would still flow from the issuer to the custodian, but the custodian could distribute them automatically to tokenholders in stablecoins or additional tokenised shares. Corporate actions such as redemptions or conversions will follow the same process, with smart contracts reflecting the custodian’s register to ensure tokenholders receive the same treatment as if they were the registered shareholder.

If regulators allowed this, a setup like this could open the door to institutional capital and still preserve the compliance standards required under fiduciary mandates.

No current offerings include these features. eToro’s plans to offer 100 US stocks using ERC-20 stock tokens will, like the others, exclude shareholder rights and investor protections.

Why is this important? Even if they want to deploy capital, institutional investors cannot act with the same freedom as retail or crypto-natives. Fiduciary obligations are non-negotiable and limit their participation until their is an underlying infrastructure that guarantees legal enforceability across the asset lifecycle.

This is where the “multi-trillion-dollar” opportunity lies, and only then will large institutional flows begin to follow and catalyse the next exponential phase of growth.

ENDS

Disclaimer: The information in this publication pertaining to Sygnum Bank AG (“Sygnum”) is for general information purposes only, as per date of publication, and should not be considered exhaustive. This publication does not consider the financial situation of any natural or legal person, nor does it provide any tax, legal or investment advice. This publication does not constitute any advice or recommendation, an offer or invitation by or on behalf of Sygnum to purchase or sell any assets. No elements of precontractual or contractual relationship are intended. While the information is believed to be from accurate and reliable sources, Sygnum makes no representation or warranties, expressed or implied, as to the accuracy of the information. Sygnum expressly disclaims any and all liability that may be based on such information, omissions, or errors thereof. Any statements contained in this publication attributed to a third party represent Sygnum‘s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. Sygnum reserves the right to amend or replace the information, in part or entirely, at any time, and without any obligation to notify the recipient of such amendment / replacement or to provide the recipient with access to the information. Simultaneously, there is no obligation of Sygnum to inform recipients of information, if before provided information later becomes outdated, inaccurate or obsolete, unless otherwise provided by applicable law. The information provided is not intended for use by or distributed to any individual or legal entity in any jurisdiction or country where such distribution, publication or use would be contrary to the law or regulatory provisions or in which Sygnum does not hold the necessary registration, approval authorisation or license. Except as otherwise provided by Sygnum, it is not allowed to modify, copy, distribute or reproduce, display, license, or otherwise use any content for commercial purposes.

Sign up for Future Finance

Join our 40,000 strong global community to future proof your investments. Sign up now to be the first to receive our news, product launches, industry reports and educational series.